The Fearful Fed?

"They’d rather go along with something that will tarnish their legacy than raise their voice ever so slightly and risk standing alone or apart for even ten minutes”. - Ryan Holiday

Highlights

What is courage? The ability to act despite daunting circumstances or uncertain outcomes. When the moment comes, does an individual stick with their spoken values or fold to the pressures of popularity? I would also say that this translates to directly confronting and facing fears.

During the Fed’s most recent speech at the Jackson Hole event on August 25th, it was indicated during his speech that inflation is still too high, they will bring inflation down to their two percent goal even at the expense of below-trend economic growth, reiterating that there is still a “long way to go”, additional evidence of above-trend economic growth threatens further inflation risks, they are acting data dependently, and they will achieve their goal for sustained growth that benefits “the people”.

Currently, the market is pricing a near zero percent probability for an additional rate hike at the September 20th meeting.

All of the most recent data since his last speech in Jackson Hole point to inflation re-accelerating, an economy that is seemingly overall “resilient”, and a tight labor market. If he does not raise rates in September, how does he have any credibility?

Consumer credit quality continues to deteriorate based on rising delinquency rates. The rising balance across all income brackets poses an additional headwind to consumer spending. Bankruptcy rates are rising and credit conditions remain tight. However, there continues to be a distortion between those data points and high yield spreads in the market. Why such a divergence between actual and historical trends?

Happy Friday!

This past week the team and I kicked off our first live Macro Madness discussion. There was a substantial amount of work leading up to that event, so I am proud and grateful for my team members. I would like to thank all of those who attended and participated in the session. Macro Optics will continue to adapt and make improvements going forward. These meetings will occur each week on Tuesday evenings at 7:30 pm Eastern time zone unless noted otherwise. If interested in our team strategy discussions and more information, sign up with the link here (https://macro-optics.com).

Today, it is appropriate to talk about courage. During last week’s Friday Reading, Game Theory, the conversation was centered around upcoming decisions that need to be made by a powerful individual. In the two-prong tree that I highlighted, neither decision has a favorable outcome for the people living in the United States. Additionally, there are external factors that influence such a decision. In this case, the recently reported data vs. the desires of powerful wealthy groups of people who use their control to influence policy decisions for a more favorable outcome for their noble status.

What is courage? The ability to act despite daunting circumstances or uncertain outcomes. When the moment comes, does an individual stick with their spoken values or fold to the pressures of popularity? I would also say that this translates to directly confronting and facing fears.

Understanding fear is a critical component of investing in markets. In my mind, there are two types of market fears.

The fear of missing out and not making money.

The fear that everything will collapse and facing financial loss.

Throughout my career, neither has been a solution for sustainably growing hard-earned capital over a long-term duration. Fear has the ability to drive the market to extremes for short periods of time before a wave of relief or rationality crashes upon the manic. Examples of the two aforementioned types of fears can be described by the dotcom bubble in 2000, March of 2009 when “the world was ending”, March of 2020 when “everybody was about to die from a global pandemic and the world was ending….again”, and crypto through February and November of 2021 where even my dog was telling me about “the next hot coin”. Dare I add, AI?

I have been reading a book called Courage is Calling by Ryan Holiday, and I highly recommend it.

A quote that I read from the book above that really stood out to me was about the actions that people take when facing difficult situations.

“People would rather be complicit in a crime than speak up. People would rather stay in a job they hate than explain why they quit to do something less certain. They’d rather follow a silly trend than dare question it; losing their life savings to a burst bubble is somehow less painful than seeming stupid for sitting on the sidelines while the bubble grew. They’d rather go along with something that will tarnish their legacy than raise their voice ever so slightly and risk standing alone or apart for even ten minutes”. - Ryan Holiday

The above is well said and is where I have drawn my inspiration for everything that I have written thus far. Specifically, in regard to the fear of missing out on financial returns for the sake of following a “silly trend”. From my experience, during that chase, a wire short circuits in people’s brains, and their minds go crazy as they are conflicted with the two types of aforementioned market fears. This is why it is important to identify and understand macro conditions. In relation to what I have seen from speculators in the crypto market who were promised life-changing wealth from some now-defunct influencers, there was no second thought to potential financial ruin. Many of those people were willing to risk everything to reach the riches that they were promised and unfortunately, I witnessed people lose everything they had. This is a sad truth and honestly brings me some pain in my heart to write.

Fed Policy

Let’s circle back to courage because now this is directly applicable to an upcoming policy decision. Currently, the market is pricing a near zero percent probability for an additional rate hike at the September 20th meeting. During the Fed’s speech at Jackson Hole, the following was stated by Jerome Powell. These are some comments that were stated during his speech delivered on August 25th, 2023.

“It is the Fed's job to bring inflation down to our 2 percent goal, and we will do so.”- Jerome Powell

“Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”- Jerome Powell

“While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.”- Jerome Powell

“Headline inflation is what households and businesses experience most directly, so this decline is very good news.”- Jerome Powell

“The final category, non-housing services, accounts for over half of the core PCE index and includes a broad range of services, such as health care, food services, transportation, and accommodations. Twelve-month inflation in this sector has moved sideways since liftoff.” In regards to non-housing services, “Given the size of this sector, some further progress here will be essential to restoring price stability.”- Jerome Powell

The Outlook: “Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.” - Jerome Powell

“But we are attentive to signs that the economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust. In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up. Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy”. - Jerome Powell

The Conclusion: ”At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all”. - Jerome Powell

The summary of this speech is that inflation is still too high, they will bring inflation down to their two percent goal even at the expense of below-trend economic growth, reiterating that there is still a “long way to go”, additional evidence of above-trend economic growth threatens further inflation risks, they are acting data dependently, and they will achieve their goal for sustained growth that benefits “the people”.

Since this speech was delivered, here is the reported data:

Headline CPI made a 2-month acceleration to 3.7% y/y (Aug) from +3.2% y/y (July).

PPI made a 2-month acceleration +1.6% y/y (Aug) from +0.8% y/y (July).

Core services ex-housing PCE +4.7% y/y (July) from +4.13% (June). This is a 1-month acceleration.

CPI core services less shelter inflation +4.1% y/y (Aug) vs. +4% y/y (July). This is a 2-month acceleration.

The price of Oil is +12.58%.

The price of Gas is +5%.

The CRB commodities index is +5.22%.

NFIB Index reports, “The net percent of owners raising average selling prices increased two points from July to a net 27%”.

“NFIB Index reports, As reported in NFIB’s monthly jobs report, 40% (seasonally adjusted) of all owners reported job openings they could not fill in the current period. Inflation and the worker shortage continue to be the biggest obstacles for Main Street.”

All of the data that is highlighted above confirms that inflation has re-accelerated for now, and the “reported” labor market conditions remain tight. The base effects for inflation do not get steeper into the end of 2023, which means inflation could likely continue to accelerate over the next couple of months or at a minimum remain persistent (holding all else equal).

As we talked about in Game Theory, there will be a decision that needs to be made. In the previous weeks, we have highlighted the re-acceleration of inflation at least temporarily, and how that is an external factor that should be influencing a powerful policymaker given his comments which he has stated publicly. Jerome Powell has stressed that they will not stop until the 2% goal is reached, they are acting in the best interest of the public, and future decisions will be data-dependent. I am not here to argue whether they should or should not hike rates. I am simply analyzing this decision in the framework of the Fed Chair’s public remarks, and decision-making process. All of the most recent data since his last speech in Jackson Hole point to inflation re-accelerating, an economy that is seemingly overall “resilient”, and a tight labor market. If he does not raise rates in September, how does he have any credibility? This is the same person who lied about transitory inflation while it went to a peak of +9% year over year during a two-year period.

Despite the new data points to support further tightening of policy based on the statements made in Powell’s most recent speech, the market is pricing a near zero percent probability for an additional rate hike at the September 20th meeting. The following quote by Ryan Holiday was mentioned above.

They’d rather go along with something that will tarnish their legacy than raise their voice ever so slightly and risk standing alone or apart for even ten minutes”. - Ryan Holiday

We discussed courage today for this very reason. Wall Street does not want another rate hike, large institutional private equity owners do not want another hike, and those who have lost everything chasing speculative assets definitely do not want another hike. There are two external influences on his decision. The data and the high-net-worth nobility. A significant amount of money was made by particular market participants during “transitory inflation”, while the disparity of wealth in the US grew farther apart. Inflation is good for those who own the right assets meanwhile the average hard-working American gets screwed.

Macro

This will be brief today, I am going to highlight the discrepancy between rising bankruptcies, declining consumer credit quality, and divergence of high yield spreads from historical data sets.

According to EPIQ Bankruptcy, commercial filings for 2023 are continuing to rise year over year. In this case, there were +634 Chapter 11 filings in August 2023 vs. +411 in August of 2022, which is a +54% increase year over year. Additionally, total bankruptcy filings increased to +41,614 for August 2023 vs. +35,409 in August of 2022, which represents an increase of +18%.

*Source: EPIQ Bankruptcy

Consumer credit quality continues to deteriorate and signs of stress are appearing in data from Bank of America. See the charts below.

*Source: Bank of America

*Source: Bank of America

*Source: Bank of America

The first chart above does not necessarily translate to declining consumer credit but wanted to note the change in consumer spending on gasoline. This is no surprise given how I have noted the re-acceleration of inflation over the last several weeks.

However, what I do think is an important takeaway is seeing the utilization rate of credit cards jump higher for the lower income bracket in chart three. This is still significantly lower than the pre-pandemic trend, but the usage is notable. Most importantly, chart two displays how credit card balances are rising across all income levels. The highest and most precipitous rise has come from the lower income bracket and could be signaling financial pressures. This is not a good combination with student loan payment resumption, prices of gas going up again, and the recent re-acceleration of inflation (for now).

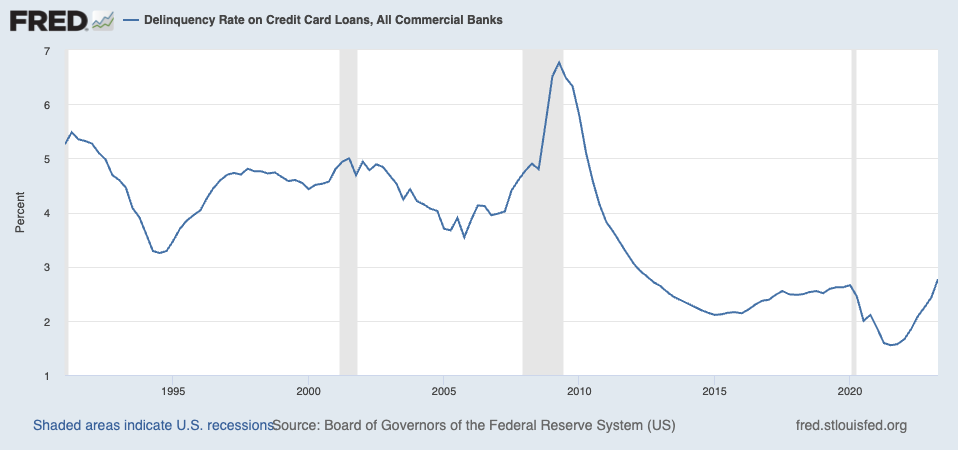

Below is a chart from Fred Economic Research of Consumer Credit Delinquency Rates.

*Source: Bank of America

Consumer credit card delinquencies continue to accelerate. The +2.77% rate at the end of Q2 2023 is the highest level since +2.71% in Q4 2012. Not only has this rate returned to the pre-pandemic level, it is now accelerating higher.

Below is a chart that I have previously published from the July 2023 Senior Loan Officer Opinion Survey which exemplifies the tighter credit standards. The cost of funds is going higher. For more information, read High Standards.

*Source: July 2023 Senior Loan Officer Opinion Survey (Higher spreads aka higher cost of capital)

Utilizing the chart above because generally, these credit conditions have a direct relationship with bankruptcies and rising high-yield spreads.

Jim Bianco does a great job of highlighting the divergence between bankruptcies and high yield spreads in his tweet and chart shown below. Link to tweet here. Additionally, give Jim a follow on Twitter because he is brilliant and does excellent research.

Source: Jim Bianco (tweet link)

Notice how generally throughout history, the green High Yield Spreads line follows the blue 3-month average bankruptcy filing. Additionally, if comparing the blue line to the credit conditions chart above from the July Senior Loan Officer survey, the correlation is visible as well.

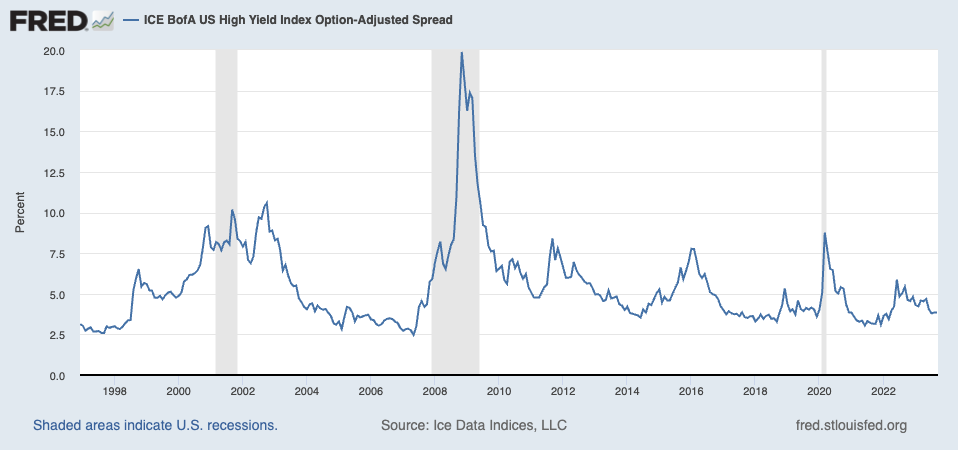

This leads me to conclude that high-yield spreads have been dramatically understated. See the chart below of High Yield OAS. When I find these types of divergences, it makes me curious about where such a market distortion of this magnitude exists.

Conclusion

Based on the recent data, regardless of whether a rate hike or not, do not be surprised by a hawkish stance by the Fed. Unless something breaks or the market crashes, there will be no rate cuts anytime soon and policy will be higher for longer. For these reasons about consumer credit along with the divergence between high-yield spreads and historically correlated data, I prefer a high-yield credit hedge (HYG) against the long side of the portfolio. This is something that I have written about previously and try to do in a timely fashion. I have been trading around this position and am looking to add back the HYG short.

We spoke about courage and fear. The connection to one another as well as the connection to markets. Fear can drive markets in short-term circumstances and at times it takes courage to execute a position. Especially a position that is very contrarian to the consensus.

The Fed has reiterated its 2% goal time and time again which seems to be ignored by the market. Currently, the market is pricing a near zero percent probability for an additional rate hike at the September 20th meeting. If the Fed is data-dependent then why would they not hike rates next week? All of the recently reported data has supported inflation re-accelerating, an economy that is seemingly overall “resilient”, and a tight labor market. If he does not raise rates in September, how does he have any credibility? This is the same person who lied about transitory inflation while it went to a peak of +9% year over year during a two-year period.

Resources

Macro Optics (https://macro-optics.com)

Chair Powell’s Jackson Hole Speech Transcript

CPI Core Services Less Shelter

tradingview.com

NFIB Index

Fred: High Yield Spreads

Bank of America: Consumer Credit Data

Jim Bianco: Bankruptcies vs. high-yield spreads

Senior Loan Officer Opinion Survey Charts (Link)

I love it when you utilize very important and relevant quotes in your writing that substantiate the behavior or psychology or other points that you are trying to make.

As always great info!