Slow Motion

Markets moving nonchalantly in a complacent direction until they don't

Highlights

The entire ISM data series decelerated meaningfully for the month of March and the “resilient” Labor market showing cracks (reviewed below).

Growth slowing + liquidity all-time lows (M2 and ODL y/y) + earnings power lower= what could go wrong?

Temporary artificial liquidity support by US treasury, however debt ceiling deadline coming quickly.

Wishing everyone a Happy Pesach and Easter this weekend! US markets are closed today, the Master’s golf tournament has taken off, and the Atlanta Braves won last night on a walk-off in the bottom of the 9th during the home opener. Going to be a good weekend!

Quick recap of this last weeks performance. SPX -0.10%, QQQ -0.9%, RUT -2.66%, Mega-Cap-Tech -0.19%, and BTC -1.08%. This is where I will give an honorable mention to the SPX positive Q1 performance, well done, because I am sure everyone that is celebrating, “bought the lows”. For reference, approximately 90% of the SPX positive Q1 return came from 7 companies and 40% of that performance came from two companies. Microsoft and Apple, which were +1.14% and -0.15% on the week. Mega-Cap-Tech continues to hold-up with market with GOOGL +4.52% this week as well, but the strength is becoming more narrow. Just say, “AI” and the companies stock price will go up.

Last week started off with a bang with TSLA deliveries miss and OPEC Oil production cuts. Price of oil and energy companies went up on that, but why is OPEC cutting production? Economic growth and demand keeps getting worse. Two other notable SPX companies received this negative message alongside a slew of poor economic data were TSLA -10.80% and DE -10.47%. Additionally, Gold ramping to cycle highs and Bonds beginning to rally are also confirming this weakening demand and growth signal. Everything is ok though, no one owns those companies anyways!

The data will be the main focus of discussion this week, and these are widely viewed metrics that are often to be considered leading economic indicators. As mentioned above, the Gold and Bond markets understand the data that I will be showcasing below, and it is my view that Equity market is ignoring these signals. I promise that I am not just cherry picking data points. If I wanted to do that, I could just cite the aggregate -26.22% EPS decline for the 16/500 SPX companies and the -76.09% EPS decline for the 5/100 NASDAQ companies that have reported earnings to date (EPS data provided by Hedgeye Risk Management). However, it is still early in the earnings season and Banks are set to begin reporting next Friday, the 14th of April.

Astonishing to look back over the last year and see how long this slowdown has taken to play out within the overall economy and markets. Perhaps I am only seeing it this way because 2022-2023 is my first time ever risk managing my capital through a real recession and bear market, but this has truly been the equivalent of watching a train wreck in slow motion (I know there have been actual train wrecks this year, please don’t cancel). Q4 2021 was as good as US economic growth could get. Since then, US growth and company earnings have gone from: “the best” to “good” to “not as good” to “should we be concerned” to “bad” and ultimately heading towards “worse” over the next few months. The 10-2 yield curve inversion has been front running that process for over a year now.

In the fall, I wrote two pieces. One is named “Labor Losses” (dated 11/18/22) and the other is named “Bad is Bad” (dated 12/2/22). In one of those publications, I discussed a key attribute to the larger recessionary outcome will be the rise in unemployment. By this point in time, it will be too late for the Fed to act “proactively”. Labor is deemed by many credible economist/ analysts such as Danielle DiMartino Booth and Joshua Steiner (Hedgeye), as the latest of late cycle indicators. Cracks are beginning to show in the overall labor market, which I will highlight in the data below.

A core aspect of this slow motion deterioration of growth and earnings as realized in actual market prices has been the incessant citation by many market participants that “bad news is good news”. First of all, I can not think of a more irresponsible way to invest money. Things are getting worse, so buy TSLA $200 calls with a one-week expiration. Things are getting worse, so buy GOOGL because they are doing super cool “AI stuff”. This in all reality equates to, “Things are getting worse, so buy any type of risk because the fed will be there to bail everyone out”. The above is a core principle of bad news= fed put (the feds intervention to prevent large market drawdowns).

Thirteen years of quantitative easing has been a real beauty for anyone who has wanted to close their eyes and allocate capital. These conditions have also created a behavioral problem where by extraordinary risks are taken with no sense of consequence because someone will always be there to bail them out. The sweet effects of QE for over a decade have numbed investors new and old to the potential risks of the QE unwind. How can I blame them when this is the way they have been trained via government intervention. This core behavior has been at the center of low volume rallies fuel by short squeezes off the low ends of trading ranges. Each one of these sell-offs over the last year has been predominantly a period of time where capital has rotated to various S&P 500 sectors. The overall markets, ex-RUT, have nonchalantly drifted sideways during this time because the real selling has not yet begun in the SPX.

Diving into the data, it is first important to understand ISM and the significance. What is ISM Manufacturing? This is a survey based on responses from the purchasing managers from 300 manufacturing firms and the data is reported monthly. Strong indicator for the level of product demand based on ordering activity. For the entire ISM series, Readings that are above 50 are expansionary, while falling below 50 is a contractionary economic signal. The data reads contractionary 46.3 (March) vs. 47.7 (February) and this equals a new cycle low. Below is a chart of ISM Manufacturing.

*Tradingeconomics.com

Next, going to discuss ISM New Orders and Employment which are both components of the overall ISM manufacturing index. What is ISM New Orders? The data is provided from the same survey as mentioned above and measures new orders placed by customers of various manufactures. This report for ISM New Orders showed a contractionary 44.3 (March) vs. 47 (February). See the chart below.

*Tradingeconomics.com

What is ISM Employment? This data comes from the same purchasing manager survey mentioned above and demonstrates fluctuations in employment at those industrial firms. The ISM Employment data printed 46.9 (March) vs. 49.1(February). Importance here is that this is not only a contractionary data point, but showing some of the first cracks within the “strong” labor market, which has been a major talking point by the fed and other market participants. See the chart below.

*Tradingeconomics.com

Concluding the US ISM series discussion is the Services data. What is ISM Services? This is a similar survey to the one mentioned above but is based on the responses of 400 purchasing/ supply executives from non-manufacturing/ services companies. For this metric, the data showcased a major deceleration of 51.2 (March) vs. 55.1 (February). While this data still remains in “expansionary territory”, this was a sharp drop off from January and February numbers.

*Tradingeconomics.com

No charts for the sake of brevity, but here are some recent economic data being reported outside the US. See the list below.

Eurozone Manufacturing PMI 47.3 (March) vs. 48.5 (February) Decelerating and Contractionary.

UK Manufacturing PMI 47.9 (March) vs. 49.3 (Feb) Decelerating and Contractionary.

German Retail Sales -7.1% year over year. 5th straight month of deceleration and 10th consecutive month negative.

China Manufacturing PMI 51.9 (March) vs. 52.6 (Feb). Slowed during last month but still expansionary.

China Services PMI 57.8 (March) vs. 55 (February). 4th straight month of acceleration into expansionary territory and a new cycle high.

Economic growth and activity are slowing globally, which has been in progress for months now. China is the only outlier in the world currently who is seeing their consumption accelerate meaningfully. After the release of the aforementioned ISM data series, the ATL Fed GDP forecast (GDPNow) has been revised lower to +1.5% from 3.5%. This is also the second revision made this week alone. They keep chasing the data lower and this is an example of the reactionary function of the Fed. They are not preemptively prepared.

*ATL Fed GDPNow

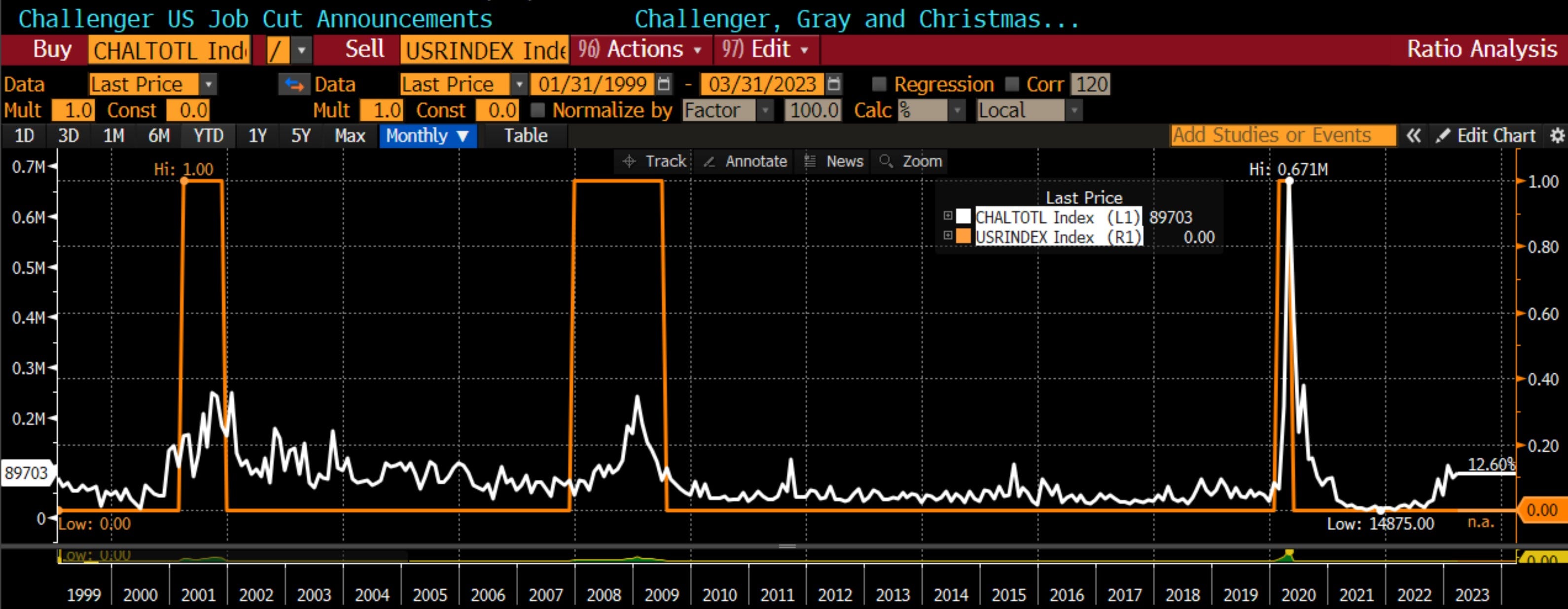

Cracks in the labor market were mentioned above via ISM Employment Index, but below I will highlight the JOLTS Job Openings and Challenger Job Cuts reports, which provide additional support to the weakening labor market and aforementioned “labor losses”. What is JOLTS? From the Bureau of Labor Statistics: Job Openings and Labor Turnover Survey, which illustrates data in regards to hires, openings, and lay-offs. JOLTS saw a decline to 9.9MM (February) from 10.5MM (January), which is good for a new cycle low.

What is Challenger Job Cuts survey? This is a way to quantify the amount of job cuts enacted by employers. This last month was slightly lower year over year, but the data series overall is trending higher. See the chart below provided by Tier One Alpha.

*Tier One Alpha

After seeing this onslaught of data, many readers may be thinking how the “expletive” in the world are the markets not cratering? Lastly, I will highlight the Artificial liquidity support is being provided by the US treasury. The pending debt ceiling has forced the US Treasury to spend out of the TGA (treasury general account) in order to keep funding the government until there is a resolution to the stalemate. On 2/3/23, I wrote a piece called, “Wrong Way” and discussed the dynamics above. Dr. Drake with Hedge Risk Management, has pointed out that “net liquidity” is the Fed’s balance sheet - (the treasury general account + reverse repos). Upon the resolution of the debt ceiling, this artificial stimulus will be withdrawn, which could pose for a rather large hangover given the Feds QT will likely still be running in the background. Comparing the “net liquidity” index to BTC and Mega-Cap-Tech with the charts below.

*Net Liquidity= Fed’s Balance Sheet -(the Treasury General Account + Reverse Repos)

*BTC

*Index: MSFT+AAPL+GOOGL+META+AMZN+NFLX+NVDA

All three of these charts are essentially the same and indicate that various assets have essentially been artificially liquidity driven in the short term. So, congrats to those feeling super “intellectual” about owning Mega-Cap-Tech in Q1 this year on some fancy AI narratives, they are all taking part in a rather similar speculation to that of BTC.

Currently, there is no end in sight to the debt ceiling solution and congress will not be back in session until April 17th. This will give them about approximately 2-months to reach an agreement before the July default deadline which has been cited by Janet Yellen. Not saying that historical performance indicates future performance, but noting that back to 2011, the SPX declined approximately -20% over a four month period of time during the previous debt ceiling debacle. For those that may not know what the credit markets think about all this, well I will post a chart below of US 5-YR CDS which was created by Hedgeye Risk Management. Effectively, the market is beginning to price in a higher probability event of a US default on its debt. Based on the CDS, an actual default probability is still low, but rising nonetheless. Throw this on top of the flames for everything else mentioned above.

*Hedgeye Risk Management

The slow motion train wreck continues to manifest in various pockets of the market (RUT/ Financials) and economic data. Specifically, ISM Manufacturing, ISM new orders, ISM Services, and Labor. Oil surprise production cuts are not bullish and was in panic out of deteriorating demand. Market performance is becoming much more narrow, and it remains a great opportunity to raise liquidity on Mega-Cap-Tech names that are rallying to lower highs. Fade the short term positive price movement incrementally. The slow motion aspect has now been supported by the artificial liquidity component from the TGA spend since December of 2022 and the SPX has nonchalantly moved sideways. TGA spend/ net liquidity arguably makes the timing of the “actual catalyst” to light the fire more difficult to pinpoint, but it is important to highlight that a very poor setup exists as the risks begin to pile on top of one another heading into an earnings season. Fuse just needs to be lit.

Happy Friday,

Aaron David Garfinkel

Resources

Hedgeye Risk Management

https://app.hedgeye.com/insights

Tier One Alpha (Challenger Job Cuts)

https://mailchi.mp/1f2d63984359/market-sit-rep-april-6th-2023-knock-out-blow?e=95ac435818

GDPNow (ATL Fed Forecast)

https://www.atlantafed.org/cqer/research/gdpnow

Trading Economics (ISM Data)

https://tradingeconomics.com/united-states/business-confidence

Tradingview

Danielle DiMartino Booth

Joshua Steiner (Hedgeye Risk Management)

Christian Drake (Hedgeye Risk Management)

Keith McCullough (US CDS Chart)

https://twitter.com/keithmccullough/status/1643976105559461888?s=46&t=pull0kgwLMsViTlT1J1vEw

Take A Breath.....Annnnnd Think, Friday Reading is free today. If this post was enjoyed or found useful, readers can let the author know that their writing is valuable by making a pledge. The author thanks the readers for their time and interest!