Similar Set

Let's discuss market expectations of economic growth vs. macro data points and a US 10-2 yield curve that just reached new cycle lows. Sprinkled in some UK-10YR GILTs for fun as well.

Highlights

ISM Manufacturing Index for June hits a new cycle low. All components of the index are in contractionary territory, which now includes the employment metric.

The theme over the last several weeks continues as economic growth slows and the yield curve hits new cycle lows of -109bps on the release of these contractionary data points. Deepest inversion since 1981.

CRB commodities index does not act like US equities and there is a notable divergence between the two asset classes. Overall, as an asset class, the index has traded in a bear market over the past several months. These three components form a similar set. Not indicative of growing demand or economic growth.

Summer!

What a time to spend time with friends, family, or both (even better)! Hoping that everyone was able to take some time off work, relax, and have a great 4th of July. I went to two different BBQs this weekend. We grilled up some Chicken Wings, Ribs, Pulled Pork, Corn, and all the other American sides. There is no place in the world like the USA (non-US readers don’t cancel), and I am blessed to live here. Completely unrelated to what we will be talking about, but in the resources section I am sharing a skit from Robin Williams acting as an “American flag” from 1982. He was truly talented.

Welcome back to Friday Reading. I say that, but some never left. The market was down over this past week, so risk manage appropriately on the short side (cover some). The economic and market setup largely remains the same. On one side of the highway, there is a drunk Fed, and on the other side is the market driving a car that is running out of gas, has a flat tire, and the driver is falling asleep at the wheel. Quite a precarious arrangement that has left many market participants out there wondering, “What happens next”. Of course, nothing may happen and these two vehicles cross paths without ever even noticing one another.

Over the last week, ISM Manufacturing reached a new cycle low, CRB commodities Index remains bearish trend/ near cycle lows, and the yield curve made a new cycle low (that is a similar set). Bankruptcies are rising and I maintain the viewpoint that volatility along with high-yield credit spreads are being understated by the market (will cover the bankruptcies and high-yield spreads next week). Given the data and historical macro confluence, hard to imagine that the aforementioned vehicles do not collide.

Macro

The market is betting on growth? We will come back to that question later. Starting off with the ISM Manufacturing report from Monday, the index printed a new cycle low. Reading 46 (June) vs. 46.9 (May). Remember below 50 is contractionary. This represents 8 straight months of contraction. Tier One Alpha highlights that 1995 was the only other period of time where there was a similar manufacturing contraction without a recession (Read Here). For readers that need a refresher on “What is the ISM Manufacturing Index”, see the link here for Slow Motion, a previous publication.

")

Tradingeconomics.com

ISM Manufacturing Prices 41.8 (June). vs. 44.2 (May)

ISM Manufacturing New Orders 45.6 (June) vs. 42.6 (May)

ISM Manufacturing Employment 48.1 (June) vs. 51.4 (May)

Note, all of the pieces of the ISM manufacturing index are now in contractionary territory. After this report was printed, commodity prices sold off, and the US 10-2 yield curve inverted to a new cycle low of -108bps.

Tradingview.com (US 10-2 Yield Curve)

Above, I have highlighted commodity prices because they are a good barometer of industrial demand and economic growth. The CRB commodity index is composed of 19 different commodities. Below is a chart of the CRB index. Cannot help but notice the divergence between this asset class and equity prices.

Tradingview.com (CRB Index)

Copper specifically is a strong indicator for industrial demand and economic growth. See the chart below. Three of the four red lines coincide with periods of US GDP acceleration. The outlier was March of 2022, however, that time period was characterized by an epic short squeeze in the equities market.

Tradingview.com (Copper)

The three factors mentioned above ISM Manufacturing, the US 10-2 Yield Curve, and the CRB commodities index form a similar set. Some readers may be tired of this by now because I have referenced the US 10-2 Yield curve in my past few publications. New cycle lows are significant and -109bps is also the lowest level since 1981. Why do I say similar set? All three of these components of the puzzle are moving at once. It is not a coincidence that the CRB index is in a bearish trend, the ISM Manufacturing, and US 10-2 Yield curve both reached new cycle lows at the same point in cycle time. This is a much larger signal about economic growth and demand.

At this point in time, it is abundantly clear that economic growth is generally slowing. However, for those willing to acknowledge, the debate continues to circulate between to what extent is growth slowing and what are the ultimate side effects. This is largely public knowledge.

There are still some outliers and others who may be living under a rock such as the Wall Street Journal. Additionally, based on the way certain baskets of assets in the market are trading and seeing flows also indicates that the consensus is chasing a “pro-growth” investment exposure. This is evident by observing the market leaders. Saying this aloud, perhaps I am in the minority in discussing the consequences of slowing economic growth. See the screenshot of a headline about “growth” below.

Wall Street Journal

Are rates up because of the prospects of future economic growth or are they up because the Move Index (bond volatility) just went vertical again over the last two weeks? An easy explanation is that Bond volatility just went vertical again. What is the MOVE Index? See the previous publication and discussion here. Two potential drivers of bond volatility currently. The UK 10-YR GILT is selling off to levels not seen since the mini-UK crisis in October of 2022. New cycle high this morning. Second, the US 2-YR yield touching cycle highs.

Tradingview.com (UK 10-YR GILT)

No one seems to talk about what was happening to the British Pound and UK pension funds the last time GILTs sold off to this level. The Bank of England had to intervene and artificially buy bonds to contain the selling to take pressure off of pension funds with a duration problem. The problem was that these funds were leveraged with lower-yielding bonds as collateral.

Tradingview.com (US 2-YR Yield)

Absolutely hearing crickets from the “Fed pivot crowd” as the US 2-YR yield returns to cycle highs and reaches the level that was realized right before SVB went insolvent. The two charts above indicate that the cost of capital is higher for consumers (such as housing) and commercial clients globally (bridge loans and long-term financing). The entire last year the popular “narrative” to buy stocks because the Fed would “pivot” and be cutting interest rates. No one talks about this anymore because they were dead wrong, and because stocks are up anyways. This prior narrative does not serve their interests at this point in time.

Not implicating these bond yields shown above and the prior history to future performance, but I do find these movements in the cost of capital to be notable. This applies more pressure to capital-intensive and rate-sensitive businesses. Lastly, I wanted to highlight these two charts as potential drivers of renewed bond volatility.

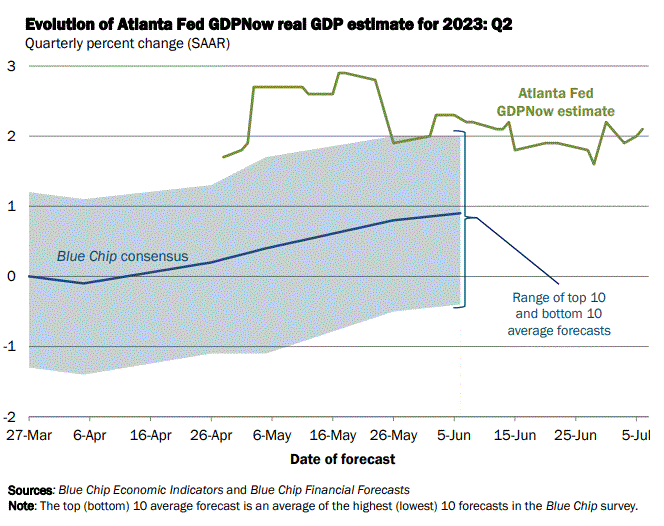

Atlanta Fed Raises GDP Estimate…..

atlantafed.org

Back to discussing economic growth. As of July 6th, the Atlanta Fed raised their GDP estimate for Q2 2023 to 2.1% from 1.9% as of July 3rd. It was not too long ago that they were slashing their GDP estimate into the actual print for Q1 2023. Throughout the first quarter, they raised their estimate to a peak of +3.5% as of 3/24/23 and ultimately cut their estimate to +1.1% by 4/27/23. Wall Street is not alone with its “pro-growth” outlook.

Conclusion

Should not be surprising to anyone at this point that economic growth is slowing especially in the industrial economy in the US and around the world. Whether that translates to the broader economy, we will have to see, history suggests that ultimately other areas of the economy will be affected. Given the abundance of negative industrial data, it is difficult to determine whether consensus is positioned for a deeper economic slowdown. My thoughts would be that they are not given their ravenous addition of “pro-growth” equity exposures and bond positioning.

The Wall Street Journal is publishing “pro-growth” headlines and the Atlanta Fed just raised its GDP forecast. While there is way more detail that goes into a real economic model, the following three signals are happening below:

ISM Manufacturing Index for June hits a new cycle low. All components of the index are in contractionary territory, which now includes employment.

The theme over the last several weeks continues as economic growth slows and the US 10-2 yield curve hits new cycle lows of -109bps on the release of these contractionary data points. Deepest inversion since 1981.

CRB commodities index does not act like US equities and there is a notable divergence between the two asset classes. Overall, as an asset class, the index has traded in a bear market over the past several months. Not indicative of growing demand or economic growth.

I cannot sit here and say when the two cars mentioned in the publication will collide or if they will even collide. What I can note is that the signals mentioned above in unison have a strong batting average historically for an unfavorable economic and market outcome. These three components form a similar set.

Happy Friday,

Aaron David Garfinkel

Resources

“Slow Motion” (Link Here)

Tradingeconomics.com ISM Manufacturing (Link Here)

Tier One Alpha 7.5.23 (Link Here)

Tradingview.com

Wall Street Journal

JP Morgan, Guide to Markets as of June 30, 2023 (Link Here)

atlantafed.org (Link Here)

“MOVE MOVE MOVE” (Link Here)

Robin Williams as the American Flag (Link Here)

Great reminder to everyone who’s complacent.

Great information! Robin Williams was so special. Love the video