Playing Positions

Moved all across the Baseball field. Same mentality applies to active market positioning. Framework of the cycle remains in tact. Will discuss M2 y/y at new cycle lows vs. inflation.

Highlights

Create ways to be flexible and adaptable within the context of the overall economic cycle.

M2 and ODL continue to decelerate and both making new cycle lows year over year.

The Fed is making decisions based on lagging indicators at very dangerous points in cycle time.

My sport of choice growing up was baseball. I played ball starting around the age of 6 and from that early age, it was always incredibly important to me to have the ability to play different positions on the field. The game was substantially more exciting when I would contribute to the team from various roles within a single game. Over the duration of an entire season, I played catcher, center field, right field, pinch runner, and pitcher. Occasionally, I would have to sit out a game to give my arm a rest. Unfortunately, I started having shoulder and elbow problems around the age of 14. Both not playing on the field and having a busted arm would drive me crazy. Hated watching the game from the sidelines. Constantly, I asked myself why, why, why about my arm. My arm was doing something completely out of my control on any given day, which was incredibly frustrating for my younger self. Amidst the anguish, I started getting myself in the game as a pinch runner on the days where I could not fully play. This was where I found a new way to alter the course of a game as the X-factor, and it was extremely gratifying. These experiences facilitated my adaptability and flexibility. My mind was set on doing whatever needed to be done to boost the team win that particular day. Every game was different and I welcomed the unknown.

Markets and Behavior

Switching to markets and behavior, how many readers that are actively trading thought that the game was easy on the short side heading into Tuesday’s and Wednesday’s close? Having fun yet? If not actively trading, I can describe the last few days as manic and emotional. An incredibly valuable lesson that I have learned from Keith McCullough and through my own personal experiences is to never short and hold. There is a “special circumstance” to every rule, but the majority of the times when I have violated this rule, the outcome was exceptionally unfavorable. That being said, I covered most of my shorts to a minimum position leading into the MSFT and META reports. Some of the readers over the last few weeks are probably thinking, “Aaron…………..all of these articles that have been published have pointed to significantly negative data points and contained proactively bearish undertones. How can he be talking about covering shorts? How is the market not crashing? This guy is full of shit”.

First, impossible to know when or if the market will actually crash and one can only infer a higher probability of such an event given the macro conditions (will discuss below). For that reason, it is important to actively risk manage short positions. As discussed in previous Friday Reading, “Truckin” (click here to review), the majority of participants are always going to be afraid of missing out to the upside. Let them chase. Second, I did take down a large portion of my short book throughout the sell-off which in turn made my long book larger for a short time period. Third, after a crazy one-day squeeze on Thursday this week, it is time to start putting it back on again incrementally to names that remain in a bearish trend. As stated in the introduction, I can play several different positions on the field.

Turns out, I got out of the way of a freight train and that was the right decision to make based on the process. Process hint: everything went down a lot for almost a week straight into catalyst events (mega-cap-tech earnings). See Crypto? Those things fell into the abyss following that airplane conversation I overheard (Friday 4/14/23) where two middle-aged men were pitching each other obscure illiquid alt coins. For now, that behavioral moment was the local top for that market. After a week where asset prices have moved violently in both directions within the current trading range, let’s look at the macro metrics.

Data

Today, the focus will be on market liquidity via money supply, CPI, and historical comparison to the relationship between the two variables. For liquidity, the study is going to incorporate M2 and Other Deposit Liabilities year over year. Updated M2 data was released this past week. This will ultimately be compared to CPI over longer periods of time. These are metrics that I have talked about before, but following up not only because these are important leading macro indicators, but the current deceleration in money supply is moving at historic pace.

The conclusion will be that Overall CPI is already well on its way moving lower and money supply year over year continues to move deeper into the negative. Credit is contracting and lending conditions are becoming tighter. The fed is focused on lagging indicators and is likely going to continue raising rates into this growth and inflation slowdown. Will be funny to see if “higher for longer” becomes what was the Fed’s late 2020-2021 “transitory inflation”.

M2 (Money Supply): What is M2? This is the Federal Reserve’s estimate of total money supply. Fundamental to study M2 given it plays a crucial role in the piece of the business cycle that is shown below. Recent chart of M2 year over year demonstrates another deceleration to a new cycle low for the month of March 2023.

Easy monetary policy→ Credit expansion→ Money supply acceleration→ inflationary pressures→ Stimulative to asset prices→ Excessive risk taking

Tight monetary policy→ Credit contraction→ Money supply deceleration→ disinflationary/ deflationary pressures→ Unwind of excessive risk taking→ Creates probabilistic outcome for total economic failure

M2

*Fred Economic Data

Another way to view Money Supply is through Other Deposit Liabilities (ODL). This is Dr. Lacy Hunt’s preferred metric to measure the real supply of money. What are Other Deposit Liabilities? The major distinction between M2 and ODL is that ODL does not include currency or retail money market funds. Below are two charts that date back to 2010. The first is total ODL and the second demonstrates the rate of change. On a year over year basis, this metric is sharply negative and decelerating at pace to new cycle lows.

Other Deposit Liabilities

*Fred Economic Data

Other Deposit Liabilities year over year

*Fred Economic Data

In other words, based on the charts above, liquidity is leaving the system and money is becoming less available on a relative basis. Credit is contracting and disinflationary pressures are in play. Given the deeply negative rate of change, it makes me wonder if CPI will follow and go negative as well, which would result in deflation by definition? Not making a “call” on that, but just something that crossed my mind. Next will talk about CPI and inflation.

CPI and Inflation: What is CPI? Consumer Price Index and measures the average change in prices paid overtime by urban consumers for a market basket of goods and services. The first chart is Overall CPI and Core CPI historically. Second chart is to focus on Core CPI, which is the aforementioned minus food and energy.

Overall CPI and Core CPI historically.

*Fred Economic Data

Core CPI

*Fred Economic Data

Overall CPI illustrated by the blue line, while Core CPI is shown by the red line. There are three observations that stand out. First, Core CPI has historically lagged the movement of Overall CPI (I encourage readers to study the charts). Overall CPI has generally peaked and troughed before Core CPI throughout history. Next, the second chart presents the two metrics over a more recent time period for a closer look. As I have previously pointed out in “Cycles Constantly Cycle” (link to reading here), Core CPI has remained much more persistent has barely moved over the last 4 months and is basically at the same rate as December 2021.

Overall CPI December 2021: 7.19% vs. 4.98% in March 2023

Core CPI December 2021: 5.52% vs. 5.6% in March 2023

The Core component is the Feds main focus. For the first time during this entire cycle, Overall CPI fell below Core CPI. Lastly, inflation falling precipitously has occurred or been a part of several recessions historically. This is shown by the shaded grey areas on the charts above. Falling inflation impacts the ability for many companies to continue growing their margins and profits. Some will lose pricing power that they have gained over the last couple years.

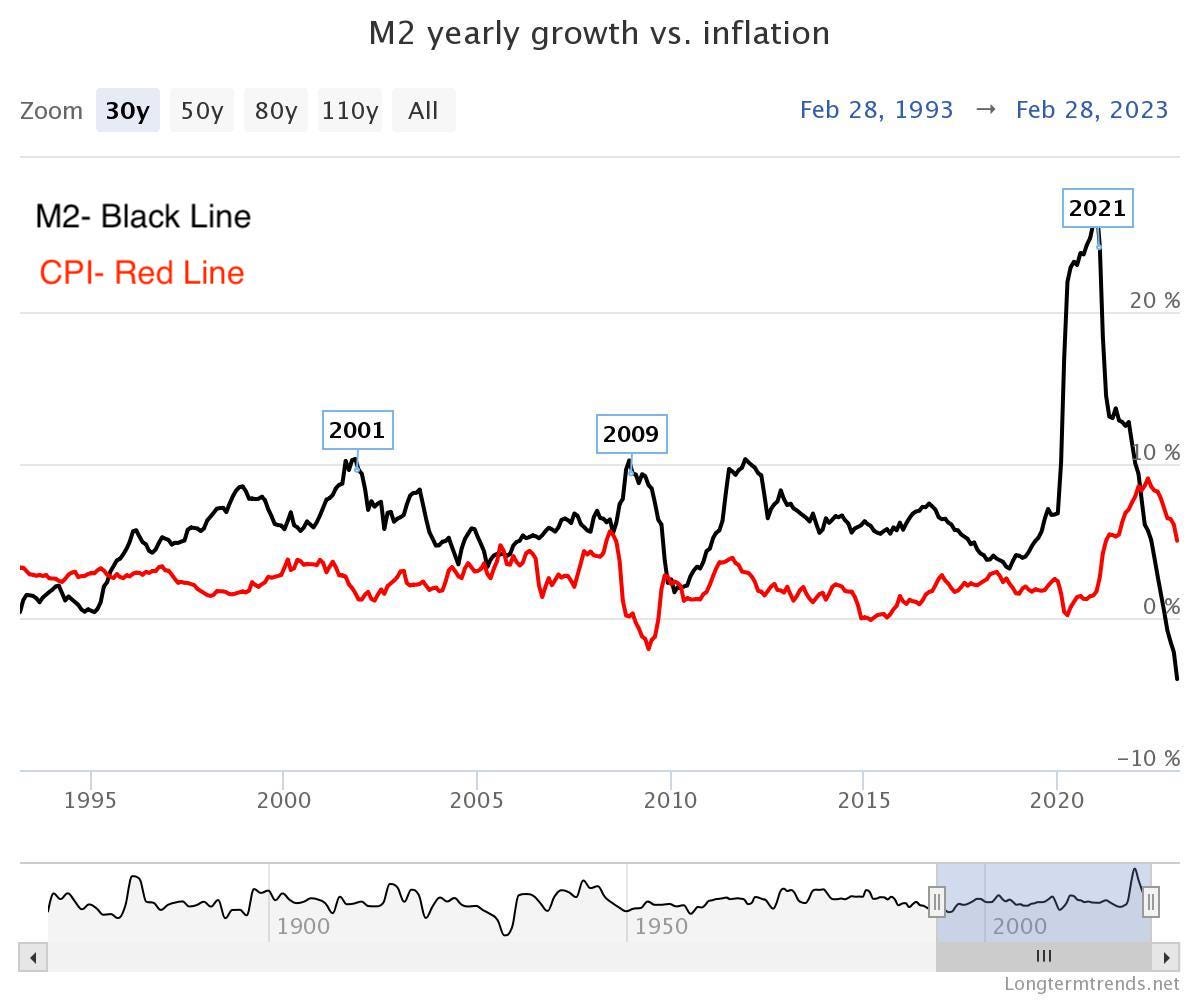

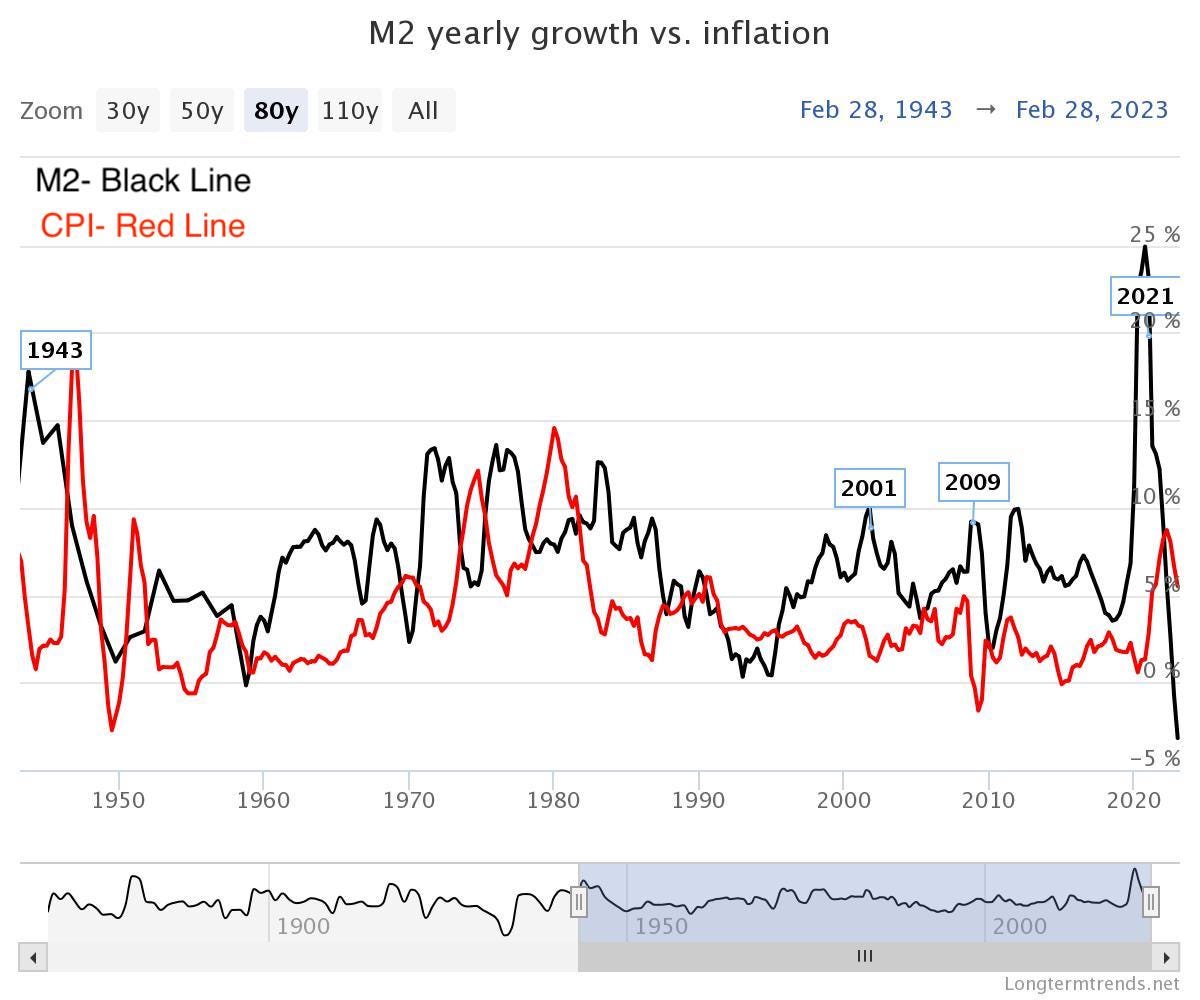

M2 and CPI comparison. The charts below are going to show the relationship between M2 and CPI over different periods of time (link for charts).

February 1993 to February 2023

Longtermtrends.net

February 1943 to February 2023

Longtermtrends.net

October 1868 to March 2023

Longtermtrends.net

By observing the charts above dating back to 1868, M2 accelerations and expansions have periodically led to higher levels of inflation. Conversely, decelerating M2 has been associated with periods of disinflation and in a few cases deflation. CPI has not lagged falling M2 every time, but this relationship can be observed throughout various points in history. Currently, there is a notable divergence between M2 and CPI. There have only 4-5 other times in US history where M2 was negative on a year over year basis. Not going to make direct analogs to any of those time periods, but all I will say is that those eras were very challenging for the markets and the people living in the US.

While Wall Street celebrates earnings beats from the top market cap companies in the US and for some on depressed estimates, there are a broad basket of stocks that compose the broader US economy outside of the 7, which contributed to 90% of the SPX Q1 2023 performance. The US economy is not Microsoft or Meta? Crazy right! The cracks are beginning to show in various retailers and cyclical “growth reliant” areas of the economy such as trucking alongside the historic fall in M2 rate of change which continues to make new cycle lows.

Wrap-up

The following is a quote that stood out to me from Hoisington Investment Management Q1 Outlook 2023. “Professors Robert J. Barro and José F. Ursúa of Harvard vigorously examined macroeconomic crises since 1870 for a broad and diverse group of countries including the U.S., the other major economic powers, and many other countries in terms of both real per capita GDP and real per capita consumption. In these crises, they found that they are not a single event but by a series of events. In other words, crisis is a process” (Link here).

Based on recent behavior, the market quickly forgets about the underlying risks. People like to point out one singular event, or headline that will lead to a market crash. They take it to youtube, “This is it! This will be the end!”, and then proceed to mindlessly shout it from the rooftops. As mentioned in the quote above, it is not about one single event but the entire series of events. I love that thought. The conclusion to the cycle will never come on the heels of one factor or event, but will be a collation of everything that transpires following a prolonged time period of excessive risk taking. This process takes time to unfold and unwind. I will be patient.

How is it possible to maintain a framework to contextualize the entire economic cycle vs. having a process to adapt shorter term movements that occur within the system?

Going back to where we started talking about playing different positions on the baseball field, this requires adaptability and flexibility. Often time, this requires taking action even though it may feel uncomfortable. Even through asset prices may have moved for one or two days out of favor of the short bias, M2 and ODL continue to decelerate and both making new cycle lows year over year. Ultimately, the Fed is making decisions based on lagging indicators at very dangerous points in cycle time and they have an unusually high batting average of striking out.

Happy Friday,

Aaron David Garfinkel

Resources

Hoisington Investment Management: Quarterly Review and Outlook Q1 2023

https://hoisington.com/pdf/HIM2023Q1NP.pdf

Fred Economic Data (click links below)

Other Deposit Liabilities (year over year)

Longtermtrends.net

Awesome information as always. I learn so much from you

Great writing. Interesting to see what happens to inflation over next few quarters.