MOVE MOVE MOVE

The MOVE Index holds significance to all markets. Spending some time discussing cross-asset volatility, while headline industrial data continues to slow and remains contractionary.

Highlights

S&P Global Flash PMI Reports are slowing around the world. The majority are in the contractionary territory and continue to move lower. New cycle lows for some of these prints and the US 10-2 yield curve heads towards cycle lows.

Move Index is bond market volatility and we discuss why this is important to follow. Currently, this metric is trending lower and will be important to monitor. Bearish volatility = bullish for the underlying asset.

Gold Vs. Bonds: Huge divergence between Gold and Real Yields. This is put into historical context, while risk and reward are discussed.

Nice Sunday Morning

Hope everyone is having an incredible weekend! There is a lot of sun, so I have been outside and have gone for a couple of runs to clear my mind. Also, been spending some time reading the book, “How to Win Friends and Influence People” by Dale Carnegie. One of the aspects that I enjoy about this book so far is how all of the lessons that Mr. Carnegie originally wrote about in 1936 are still applicable today, almost 100 years later. Additionally, there is a substantial amount of history embedded within the book. Here is a quote that I appreciated by Ralph Waldo Emerson, “Every person I meet is my superior in some way. In that, I learn of them”. This really speaks to remaining humble, having an open mind, and maintaining a willingness to always learn something from others regardless of their origin/ appearance. The lesson above most certainly applies to the Harley Bassman interview excerpt (full interview in resources) that I am sharing below. Highly recommend reading or listening in some spare time.

Today’s “Friday Reading” is being published on Sunday, so much for “Friday Reading”. By the time viewers are reading this note, over the weekend, the Twitter and media sphere has moved from being “submersible experts” to “Russian military coup experts”. This type of behavior is not too dissimilar from the permanently bullish equity strategist jumping from talking point to talking point and searching for their next catalyst narrative. Remember, Wall Street is in the business of selling stock. In recent weeks, there has been a notable Wall Street Equity Strategist, who has won the “year-to-date” game and has proclaimed that the next catalyst for the market will be a re-acceleration in PMI numbers and economic expansion.

Two details. One is, do not ask how this strategist did during 2022. Second, while many market participants spend time this weekend focused on AI, the latest crypto market pump, and/ or whatever the hell is happening in Russia, we will be focused on the numbers. Sneak peek, Manufacturing PMI data is unequivocally slowing around the globe to relative lows and new cycle lows in some areas. In last week’s Friday Reading the 10-2 yield curve was highlighted in “Stock Pitches and Economic Ditches” and during this past week, the metric fell another -6bps to a total inversion of -101bps. Back towards cycle lows (similar to US Manufacturing PMI). Additionally, “Net Liquidity”, declined -158.8B (-2.53%) and is the largest 1-week drop off since the week of April 17th (see conclusion and resources for “Net Liquidity” explanation).

Macro

Thursday/ Friday, June 15th/ 16th, the market found itself in a call-buying frenzy and investor sentiment was reaching levels of peak euphoria. Fading those extremes and raising more cash proved to be a prudent strategy on the short side over the past week. The major indexes were down the majority of the week, which provided the opportunity to cover some of those short positions if actively trading. If not active, that is perfectly fine. Enjoy the ride. Let’s move into the data.

S&P Global Flash PMI Reports- Predominately slowing across the board. See detail below. This past week, the UK raised their central bank rate by a “surprise” 50bps to a rate of 5%. The ECB has shown no sign of ending future rate hikes. Additionally, the US Fed plans on raising rates again in July. In effect, the largest central banks around the world are continuing to raise rates and tighten monetary conditions into an economic slowdown (most specifically industrial/ manufacturing recession). The cost of capital is going higher and remains elevated. Just as a reminder, it was only 6-months ago that consensus was adamant that there would not be a recession in Europe.

United States Manufacturing PMI: 46.3 (June) vs. 48.4 (May)→ 2-month deceleration back into contractionary territory (below 50) and toward Cycle Lows.

Tradingeconomics.com: United States Manufacturing PMI

United States Services PMI: 54.1 (June) vs. 54.9 (May)→ 1-month deceleration.

Eurozone Manufacturing PMI: 43.6 (June) vs. 47.1 (May)→ Contractionary (below 50) and 5th straight month of deceleration to a New Cycle Low.

Tradingeconomics.com: Eurozone Manufacturing PMI

Eurozone Services PMI: 52.4 (June) vs. 54.5 (May)→ 2nd straight month of deceleration.

Australia Manufacturing PMI: 48.6 (June) vs. 48.4 (May)→ 2nd consecutive month of acceleration, but still in contractionary territory (below 50).

Australia Services PMI: 50.7 (June) vs. 52.1 (May)→ 2nd straight month of deceleration.

Japan Manufacturing PMI 49.8 (June) vs. 50.6 (May)→ Contractionary (below 50), however trending higher in a positive direction.

French Manufacturing PMI 45.5 (June) vs. 45.7 (May)→ Contractionary (below 50) and 5th straight month of deceleration to a New Cycle Low.

French Services PMI: 48.0 (June) vs. 52.5 (May)→ Contractionary (below 50) and 2nd straight month of deceleration to a New Cycle Low. This metric has fallen precipitously over the last two months and is one of the first contractionary “Services PMI” prints that I have seen since the fall of 2022.

German Manufacturing PMI: 41.0 (June) vs. 43.2 (May)→ Contractionary (below 50) and 5th straight month of deceleration to a New Cycle Low.

Tradingeconomics.com: German Manufacturing PMI

German Services PMI: 54.1 (June) vs. 57.2 (May)→ 1-month deceleration.

UK Manufacturing PMI: 46.2 (June) vs. 47.1 (May)→ Contractionary (below 50) and 4th straight month of deceleration.

UK Services PMI: 53.7 (June) vs. 55.2 (May)→ 2nd straight month of deceleration.

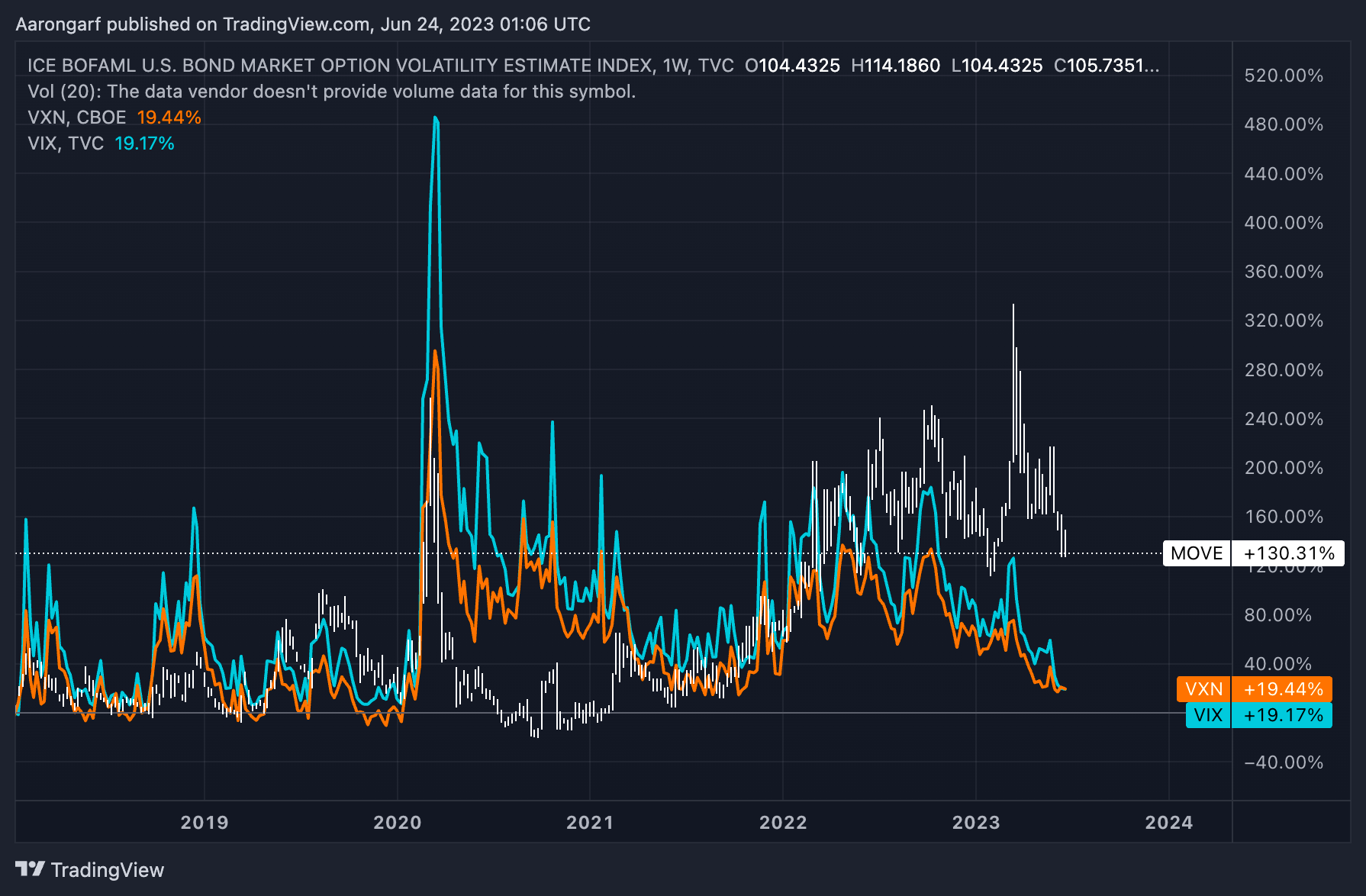

MOVE Index

Going to discuss bond volatility and show a chart below. Given that slowing global industrial growth has been clearly established along with the 10-2 yield curve moving towards cycle lows, makes sense to talk about bonds. First, what is the Move Index? The MOVE is a benchmark for US treasury market volatility, and the index is based on 1-month treasury options weighted for 2, 5, 10, and 30-year contracts. The index was created by Harley Bassman and captures the implied volatility of the bond market.

See the following explanation from the creator, Mr. Bassman, during an interview with Phill Galdi (ICE). Click the link here or see the resources section to read or listen to the full interview.

“The MOVE and the VIX are very similar in that they basically measure short dated one month volatility. The key thing is that these indices are mostly coincident indicators as opposed to forward looking, because they tend to track realized volatility. There's a very tight correlation between the realized movement, the day to day market activity of liquid instruments, and options on them.

Why the MOVE was so valuable recently is that, while the VIX and equity markets get all the headlines; the bond bucket is actually much bigger, and it tends to signal things ahead of the equity market, because the underlying plumbing of finance happens in the bond market. Although the VIX went up a lot, the MOVE went up awful a lot more and that really told you that this was a serious problem in the market, because bonds should not move more than stocks do.” -Harley Bassman

Tradingview

Citing the MOVE this week, because this metric has been trending lower over the last couple of months. Why is this relevant? It is always important to pay attention to volatility because bearish volatility is generally bullish for the underlying asset class. In this case, the asset class that we are discussing is US Treasury Bonds. Still early to determine, but want to highlight the thought as this is something on my radar. Slowing growth is positive for bonds and if bond volatility continues to fall lower, that would create another layer of positive conditions for US Treasury Bonds.

However, I remain skeptical about this recent fall in bond volatility and if it is more circumstantial to volatility falling for most asset classes across the board (specifically equities). The chart below shows the MOVE index (white) in relation to the VIX (S&P 500 volatility in light blue) and VXN (NASDAQ volatility in Orange). Notice how these volatility indexes generally trade alongside one another. There is a significant divergence that becomes much more obvious following the SVB collapse in March of 2023. Bond volatility became a driving force behind elevated equity volatility throughout 2022 and the most rapid Fed rate tightening cycle in history.

Tradingview

Next, the chart below demonstrates the previous correlation between TLT (long-dated US Treasury ETF) and the SPX along with QQQ. Going back to the summer of 2021, these three traded in a similar manner and then even suffered comparable drawdowns during 2022 through the course of elevated bond/ equity volatility shown above. At the beginning of 2023, the divergence between the equity and bond ETFs began to develop. Following the SVB collapse in March of 2023, the divergence became significant and more pronounced. Below, see QQQ (orange), SPX (white), and TLT (light blue).

Tradingview

The showcased divergences create an interesting setup because equity volatility is potentially being understated by the market, or perhaps bond volatility is being overstated. Non-withstanding, the slowing growth mentioned above is generally a positive condition set for US Treasury Bonds and is unfavorable for equity prices.

In the event that bond volatility continues to trend lower from here, US Treasury Bonds become a potentially asymmetrical portfolio position. They are also in an asymmetric position for a type of tail risk market crash where the only assets that will go up in value during those conditions are likely US Treasury Bonds and US Dollars. During this period of time, elevated bond volatility would probably not matter for the long side. While it is still early for the bond volatility observation, at the moment (and this can always change), the 30-YR yield is showing the most promise on the long side.

The biggest risk to bonds is if there were to be a re-acceleration of inflation. Following June, the inflation comps could begin to get easier on a year-over-year basis. Primarily from the energy complex, which went through the Russia-Ukraine Oil shock in March and June of 2022 where Oil was $120ish versus the $69 spot price today. The energy component of inflation generally flows into CPI at a 1 to 2-month lag. This is something that I have learned from Josh Steiner, Analyst, at Hedgeye Risk Management. In this case, the tougher inflation comps, have led to headline CPI falling precipitously in H1 2023 and could become much more difficult starting August H2 2023.

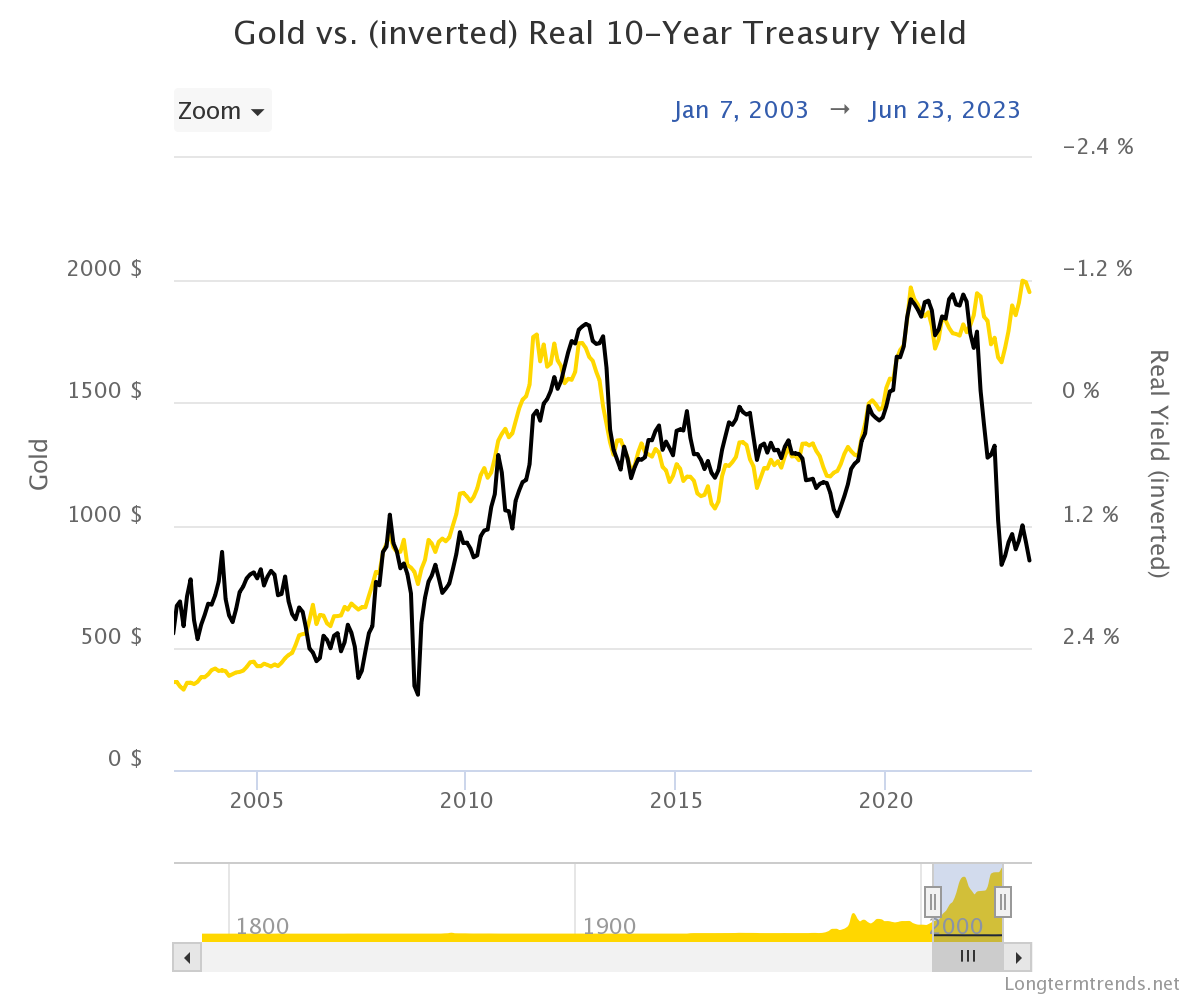

Gold Vs. Bonds

Gold historically trades inversely to interest rates and as a bond proxy. Interest rates/ Real Yields up = usually Gold down. This asset also performs better under the slowing economic growth condition set. Bonds and Gold both stand to benefit if there are higher levels of unemployment in the future. Additionally, Gold stands to benefit from falling bond volatility (MOVE Index) as well. Hedgeye Risk Management has also done an excellent job pointing out the relationship between Gold and Real Yields. Disclosure and not investment advice, I added to my Gold long position Thursday this past week.

What are Real Yields? The real interest rate is the difference between the nominal interest rate and the actual/expected inflation rate. The “Real Yield” in the chart below is calculated by subtracting the 10-Year (expected) Inflation Rate from the 10-Year Treasury Constant Maturity Rate, according to longtermtrends.net. Example: (10-Year Treasury rate of 3.80%) - 10-YR (expected inflation rate of 2.22%) = Real Yield of 1.58%.

Longtermtrends.net

Another notable divergence stands out currently (2023) here in the chart above. There have been other periods of time with similar divergences, however, none were this extreme. Throughout 20 years of history, those years were: July 2007, February 2011, and November 2018. Perhaps Gold is attempting to signal something that the treasury market has not realized yet.

One of the biggest risks to gold (aside from the re-acceleration of inflation) is that it acts as one of the only sources of liquidity during deep market drawdowns. In other words, if there were a real panic in the financial market where there is indiscriminate selling of assets, Gold becomes a source of liquidity as fund managers are selling “what they can sell” in order to meet liquidity/ capital requirements. During that chaotic market environment such as the Fall of 2008 and March 2020, Gold sold off while US Treasury Bonds and US Dollars appreciate for a brief moment in time. However, on the other side of the deep panic selling, lies inevitable US credit expansion and inevitable currency debasement. Historically, that has proven to be a favorable environment for Gold.

Conclusion

Sometimes there will be a “Not Friday Reading” that comes my way. In this case happy Sunday! It was nice to have some more time to think because generally, I write these two hours before the market opens on Friday morning. The thought exercise is fun and I am still working on getting my time down.

Manufacturing PMI data is unequivocally slowing around the globe to relative lows and new cycle lows in some areas. In last week’s Friday Reading the 10-2 yield curve was highlighted in “Stock Pitches and Economic Ditches” and during this week, the metric fell another -6bps to a total inversion of -101bps. Back towards cycle lows. Additionally, “Net Liquidity”, declined -158.8B (-2.53%) and is the largest 1-week drop off since the week of April 17th. If a refresher is needed on the explanation of “Net Liquidity”, read “Lower Liquidity” and “Slow Motion” where this topic was previously discussed in more granular detail.

The MOVE Index was discussed and highlighted the divergence between equity and bond volatility. Important to pay attention to volatility because bearish volatility is generally bullish for the underlying asset class. Over the last couple of weeks, US Treasury bond market volatility has been trending lower, so keeping an eye on that metric and trend.

Gold shows a wide divergence between the spot price and Real Yield, which historically demonstrated an inverse correlation. Perhaps there is a deeper signal embedded within this divergence. Gold and the yield curve understand that growth is slowing.

Highlighting these three items today because this is what has been on my mind while the masses seem to be gravitating toward noisy headlines and vertical asset prices. Every day is a new day and the game always presents a new opportunity. Mistakes and failures are learning lessons and a part of the humbling education of the market. Just keep moving forward.

Happy Sunday,

Aaron David Garfinkel

Resources

“How to Win Friends and Influence People”- Dale Carnegie (Link Here)

Tradingeconomics.com

Tradingview.com

Harley Bassman Interview (with Phil Galdi, ICE)

Hedgeye Risk Management (Website Link Here)

Gold vs. Real Yields Longtermtrends (Chart Link Here)

Josh Steiner, Analyst, Hedgeye Risk Management (Twitter Handle Here)

“Lower Liquidity” and “Slow Motion”

Very insightful as always! Enjoy the rest of your Sunday