Is Anyone There? *Echos*

Discussing rising bankruptcies, real-life investor sentiment, and Google Search trends for hot market buzzwords.

Highlights

Chapter 11 bankruptcies filed in the first half of 2023 accelerated +68% year over year. Consumer credit card delinquency rates continue to accelerate. Risks are underestimated by the high-yield market with high-yield credit spreads being understated.

Tighter monetary policy→ Raises the cost of capital→Tighter credit conditions→Slows economic growth→Hurts profitability→Higher credit spreads→Company inability to refinance or pay off debt obligations→Rising Bankruptcies→Tighter credit conditions→Higher credit spreads

Google search interest for buzzwords such as “AI” and “Chat GPT” is waning, while also diverging from related equity prices.

Weekend!

Per usual, it is extremely nice to wake up this morning and have a nice cup of coffee. Never underestimate the importance of a swift burst of energy during the early morning hours. Besides, I cannot be all drowsy this morning when I walk over and start shouting into a well about how, “market volatility and high yield credit spreads are being understated”, or how, “Industrial growth is contracting globally”. By now, I am sure that sure no one is listening, so I will yell one more time for good measure, “CPI and PPI falling year over year in cannonball formation are negative for corporate profits”!

A funny observation that I have made is that the current market conditions are the exact opposite of February/ March of 2021. For readers that do not know what was happening in the market around that time, I recommend referencing a chart of BTC or ARKK. February/ March of 2021 could be characterized by accelerating growth, accelerating inflation, and credit expansion. Meanwhile, the current condition set based on the incoming data is slowing growth, slowing inflation, and credit contraction. Easy monetary policy vs. tight monetary policy. Yet, the market is trading in a very similar manner (price action and sentiment) in comparison to that period of time. The only analogous factor that I can draw between the two time periods is the influence of positive net liquidity. However, as noted in my publication “Lower Liquidity” (Link Here), that dynamic in 2023 to date has ended post-US debt ceiling resolution.

Often, I enjoy gauging “sentiment” through my real-world interactions with other market participants. Last night, I had a friend text me about XRP crypto being back. This is the first time that I have heard him mention this asset in over a year. At dinner this week with one of my close friends, confidently told me about how he was up more than +100% returns on all of his stock picks for the year. Every one of the names was a profitless tech company. Lastly, I am now starting to overhear people on my office floor talking about their stock picks once again. Even heard some people “cheering” as the price of their favorite assets went higher intra-day. Have not heard anyone say a word on my floor about their investments in over a year. Not making any assumptions or implications based on those experiences, but I find the behavior notable.

Last week, we discussed slowing economic growth and today I will share thoughts about some of the potential side effects such as lower corporate profits as it translates to rising bankruptcies. For fun, at the end of the publication, I will present some charts from google trends that demonstrate the trajectory for interest in words such as “AI” and “Chat GPT”. Inflation data received this week along with the Fed’s likely path forward to continue raising rates into the next policy meeting, builds a stronger case for the aforementioned side effects.

Macro

Perhaps we can dive into more detail about global PPI data next week, but the summary is that PPI in the Eurozone and China is in deflationary territory. This happens when the metric goes negative on a year-over-year basis. US PPI this week printed at +0.1% (June) vs. +0.9% (May). This is on the precipice of negative territory, but we will see what happens as the base effects for inflation dramatically ease going forward. In other words, it starts becoming much more difficult for inflation to fall off a cliff from here if all else remains the same.

Companies benefitted from accelerating inflation on the way up because they were able to keep raising prices and the higher costs were absorbed by consumers. Now with inflation slowing, it becomes much more challenging for some companies to continue raising prices at the same rate as in 2021/2022. For many companies, this could be the moment when things are as good as it gets and they have locally achieved peak pricing power.

How does this pertain to bankruptcies and high-yield credit spreads? The loss of pricing power and the prospect of lower profitability increases the risks for already unprofitable and cyclical companies. As this happens, the debt should be priced accordingly. Meaning, more risk = higher credit spreads, which equates to a higher cost of capital overall. For some companies, the lower profitability could even put them out of business (Bankruptcy). This is another contributing factor to higher credit spreads. More bankruptcies = more risk for comparable companies = higher credit spreads.

Inherently, this may even create a self-sustaining negative feedback loop. One which looks like the following:

Tighter monetary policy→ Raises the cost of capital→Tighter credit conditions→Slows economic growth→Hurts profitability→Higher credit spreads→Company inability to refinance or pay off debt obligations→Rising Bankruptcies→Tighter credit conditions→Higher credit spreads

Bankruptcy Data

According to Epiq Bankruptcy, there were a total of 2,973 total commercial Chapter 11 bankruptcies filed in the first half of 2023. This is a +68% increase year over year in comparison to the 1,766 filings in 2022. Total individual filings were up +17% year over year (205,313 vs. 175,094) for the first half of 2023.

")

EPIQ Bankruptcy

Overall commercial filings were up +18% year over year (1H 2023: 12,107 vs. H1 2022: 10,258). Additionally, total bankruptcy filings were up +17% year over year (1H 2023: 217,420 vs. 1H 2022: 205,313)

The trend for bankruptcies has been rising, however recently, the market has been understating future risks for lower company profitability and individual consumer credit based on current high-yield credit spreads. The real kicker within the observable data sets is that rising unemployment has yet to play a role in the already deteriorating consumer and company credit conditions. We will see whether that ultimately becomes a factor in the markets, but the Fed’s goal has been to achieve higher levels of unemployment in order to contain inflation. With that goal in mind, they continue to raise rates at a very dangerous point in the cycle.

JP Morgan Guide to Markets Q2 2023

Note in the chart above the relationship between the default rate and rising high-yield spreads. In this chart, it is known as “spread-to-worst”, which is the grey line. The blue line represents the default rate. Historically rising high yield spreads and the default rate has coincided with recessionary periods that followed. Note that it does not always immediately happen overnight.

Since we mentioned consumer credit, below is Chart 1 of a 20-year history of delinquency rates on credit card loans and Chart 2 compares delinquency to the unemployment rate.

Fred: Delinquency Chart 1

Fred: Delinquency vs. Unemployment Rate Chart 2

Delinquency rates have steadily been rising off of their post-pandemic liquidity flood lows. This is to be determined whether the recent trend continues or if it is more of a normalization in the delinquency data. Chart 2 shows that rising delinquency at certain points in cycle time precedes higher levels of unemployment, however, this is not a perfect relationship.

AI Related Google Search Trends

None of the observations below should be taken out of context. This is just a study of Google search trends as a gauge of interest in various search terms and topics. What I do find interesting is that many of these terms peaked in search interest at very particular points in market time. I am not going to reference each point, so will leave that up to the readers for self-study.

The first is Bing, which was one of the first names to gain interest and also the first one to peak right around the early February short squeeze (one of the largest in the last decade).

Google Search

Chat GPT worldwide peaked in late March and early April. This has been declining since

Google Search

Chat GPT in the US peaked secondarily in late April and has declined since.

Google Search

The term “AI” in the US peaked around the week of April 16th to April 22nd. This one, in particular, is my favorite because it lines up with the conversation that I overheard on an airplane on April 14th where two gentlemen were pitching each other their super intellectual “AI stock picks”. I reference this experience in my publication “Truckin” (Link Here).

Google Search

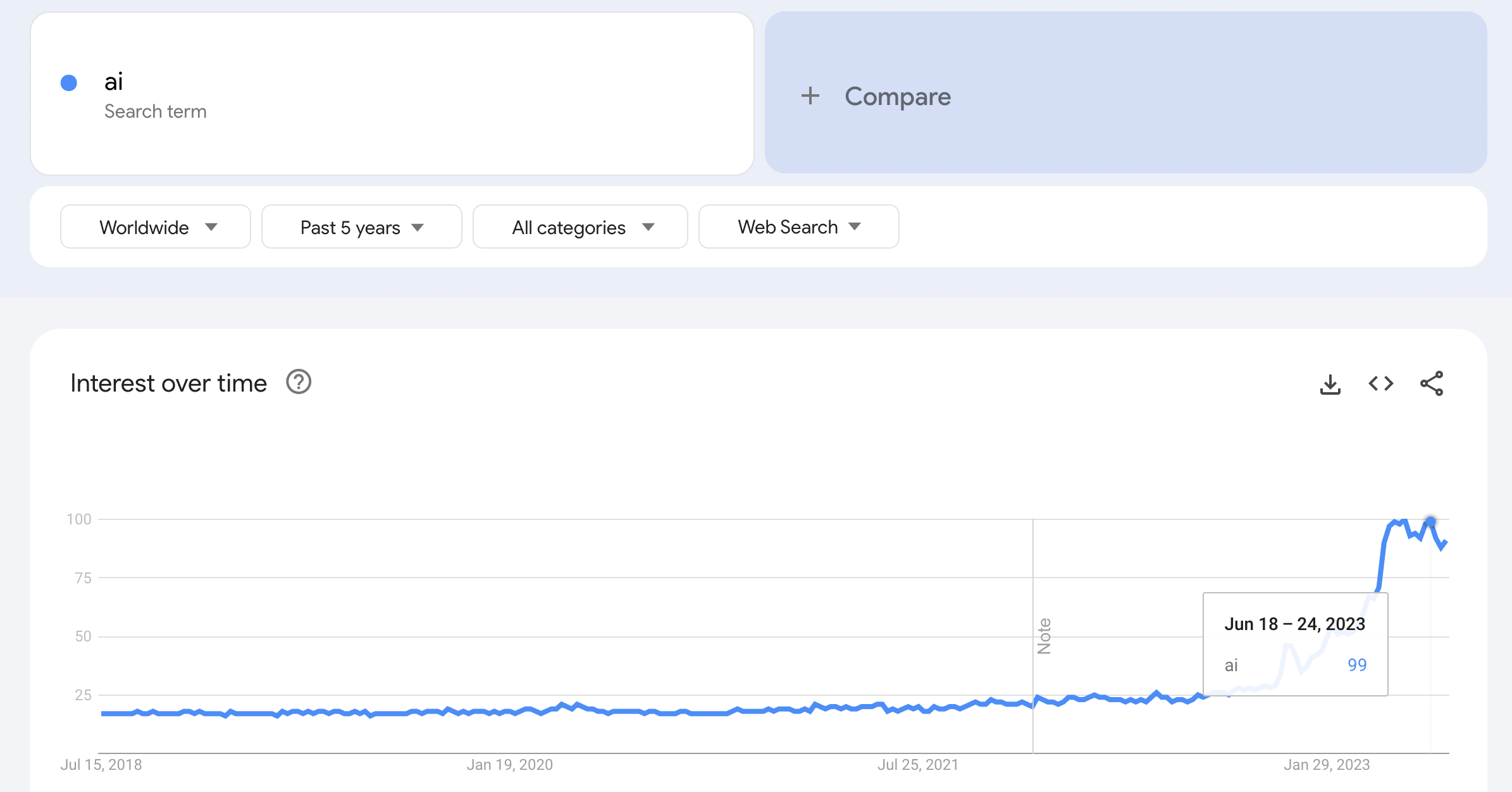

Here is the search term for “AI” globally which has remained more resilient, but has locally peaked during the week of June 18th to 24th.

Google Search

Below is a chart in search interest for ARKK, which I mentioned at the beginning of this publication.

Google Search

Below is a chart for search interest of “Dogecoin”, which is a well-known meme and crypto bubble.

Google Search

There are no inherent conclusions from this data other than the interest in some of these buzzwords that have been driving market sentiment and profitless tech higher is potentially waning. One particular detail that is worth mentioning is that there has been a recent divergence between the search interest data going lower and tech/AI-related stocks going higher.

I make a comparison between February/ March of 2021 and the first half of 2023 in terms of price action and sentiment. The latter two charts of AI and Dogecoin do an excellent job of quantifying that statement in terms of search interest. A big takeaway from the Dogecoin chart is that just because something peaks in interest does not mean there cannot be a re-insurgence.

Most notably, the peak in ARKK search interest came at a time when Cathie Wood was receiving record amounts of allocations and fund flows into her ETF (ARKK). This peak in search interest also coincided with the peak in the asset price for what has turned out to be one of the greatest bubbles since NASDAQ during dotcom.

Conclusion

Chapter 11 bankruptcies filed in the first half of 2023 accelerated +68% year over year. Consumer credit card delinquency rates continue to accelerate. This is happening all the while there has been no lift in the unemployment rate to date. Risks are underestimated by the high-yield market with high-yield credit spreads being understated.

Tighter monetary policy→ Raises the cost of capital→Tighter credit conditions→Slows economic growth→Hurts profitability→Higher credit spreads→Company inability to refinance or pay off debt obligations→Rising Bankruptcies→Tighter credit conditions→Higher credit spreads

Google search interest for buzzwords such as “AI” and “Chat GPT” is waning, while also diverging from related equity prices. I cannot help but notice and draw parallels between the price action and sentiment between the first half of 2023 and February/ March of 2021. The greatest divergence between those two periods of time is the opposite macro condition sets.

This is not investment advice, but just how I am managing my own portfolio. My view is that I still find the continued strength in equity prices as a great opportunity to raise cash and add emphasis to acting incrementally. Thursday during this week’s rally, I sold my SPY position in my long-only account. As stated, high-yield credit spreads are potentially being understated significantly given the inherent market risks, so this week I have hedged my long portfolio Thursday by adding short exposure via HYG (high-yield credit ETF). This was an easy place to start acting incrementally on the short side. If actively managing, remember the importance of not shorting and holding. A couple of weeks ago, I mentioned that I had been covering short positions at the recent lows. That was a prudent decision because now I can add the hedges back and in some cases at an even better price. Best of luck out there.

Happy Friday,

Aaron David Garfinkel

Resources

EPIQ Bankruptcy (Link Here)

Delinquency Data (Fred Link Here)

Fred Delinquency Data vs. Unemployment (Link Here)

Google Trends (Link Here)

“Lower Liquidity”- Aaron David Garfinkel (Link Here)

“Stock Pitches and Economic Ditches”- Aaron David Garfinkel (Link Here)

JP Morgan Guide to Markets Q2 2023 Asset Management Report (Link Here)

Truckin (Link Here)

Good Points. I just raised our cash level from 10% to >20%. If the market keeps moving higher then we’ll still participate, just not as much. And if it weakens: dry powder! … Regarding lofty tech stock prices, your readers may want to look at the MSFT high price in 2000 and how long it took the company to beat that old mark. I think it was 2016 before it hit new highs. The company did fine during those 16 years as far as revenues and earnings went, it just took a while for them to catch up with an absurd stock price. A reasonable person could argue a lot of tech companies today are on the same footing as MSFT in 2000. On a happy note, MSFT is up 5-fold or 6-fold since that new high in 2016. That new high was a buy signal.

As always, very informative