High Standards

Senior Loan Officer Opinion Survey indicates tighter credit conditions and weaker loan demand. I will also discuss Estate and an example that I have created.

Highlights

Extend and pretend is the name of the game? How long can this type of behavior continue in the debt markets? The cycle seems to be moving at a glacial pace and numbers for Real Estate deals simply do not work right now.

Credit standards are tighter and the cost of capital is higher. This impacts borrowers’ abilities to refinance their existing debt. If collateral values fall further then that poses an even greater threat specifically in the Real Estate markets.

Imagine a world where rates are higher because of actual supply and demand. People still need debt; however, credit standards are tighter and credit is less available. What happens when the supply of something is constricted? It becomes more expensive.

Weekend Is Here!

Pull up a chair, and let’s watch some paint dry! I got off the phone yesterday with one of my good friends from grad school. She is involved in Real Estate as well at the “fund” level, and we were both talking about the surprising pace at which this cycle is moving. She mentioned, “We keep saying that the next shoes will drop imminently, but seems that the can keeps getting kicked down the road”. During this conversation, I noted the discrepancy between the buyer’s asking price, the seller’s asking price, and the way the numbers work in the lender’s model.

When the numbers simply do not work for almost any deal, something has to give at some point in time. We contemplated whether this is just our perception solely because of our limited years of experience in the industry (starting in 2019) or if reality is really moving that slowly. For more experienced Real Estate veterans (that are readers), please feel free to comment and compare now vs. prior cycle experiences. Would love to hear the wisdom and share it with other readers. As with anything in life, we measure the magnitude of our experiences against what we think we know to be true.

Today we are going to discuss bank lending standards and the cost of capital.

Macro

Previously, I have mentioned the tightening of credit standards and expressed that high yield spreads are being understated when considering the inherent market risks. This is one of the reasons why I have stated that a high-yield credit short position is a reasonable hedge for a portfolio. If trading actively, HYG just dropped off a cliff this week, so book some gains there. Putting that aside, let’s discuss a way to measure credit standards and availability. We will look at the Senior Loan Officer Opinion Survey for the month of July.

What is the Senior Loan Officer Opinion Survey? According to the Board of Governors of the Federal Reserve System, this is a survey of up to eighty large domestic banks and twenty-four U.S. branches and agencies of foreign banks. The Federal Reserve generally conducts the survey quarterly, timing it so that results are available for the January/February, April/May, August, and October/November meetings of the Federal Open Market Committee. The Federal Reserve occasionally conducts one or two additional surveys during the year. Questions cover changes in the standards and terms of the banks' lending and the state of business and household demand for loans. The survey often includes questions on one or two other topics of current interest.

The survey reads as follows, “Regarding loans to businesses, survey respondents reported, on balance, tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the second quarter. Meanwhile, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories”.

Additionally, here is the survey’s outlook, “Regarding banks' outlook for the second half of 2023, banks reported expecting to further tighten standards on all loan categories. Banks most frequently cited a less favorable or more uncertain economic outlook and expected deterioration in collateral values and the credit quality of loans as reasons for expecting to tighten lending standards further over the remainder of 2023”. Again, this is according to the Board of Governors of the Federal Reserve System (link here).

Putting this simply, credit is becoming more difficult to obtain, and the demand for new loans has fallen. The outlook is for this trend to continue to get worse. Higher cost of capital and tighter credit standards. Why is this important? Because, there is a direct relationship between credit growth, investment, and the following impact on real economic growth. In the outlook, I find it interesting that they cite the, “expected deterioration of collateral values and the credit quality of loans”. This is directly what I am citing in my introductory paragraph where the numbers just do not make sense right now.

A quick example of this in the real estate world is if someone buys a real estate property for $100,000,000.

They take out a 2-YR loan of $70,000,000 or 70% loan to value (LTV) to buy the property. This type of leverage was common over the last four years. The initial rate may have been 2.5%.

Let’s say the value of the collateral has fallen to $80,000,000 (-20%).

The current loan of $70,000,000 would represent 87.5% LTV. The leverage point increased.

2-years have passed and now the borrower needs to refinance their $70,000,000 loan.

Rates are higher and credit standards are tighter. The bank only wants to lend at 65% LTV. Assuming this is multifamily, the rate may be 5.5%-6% on the new loan.

Based on the updated valuation, the borrower would only be able to receive a loan of $52,000,000 for their property, and the cost of capital has doubled.

This leaves them with a -$18,000,000 shortfall to pay back their existing debt.

I will say this is somewhat of an exaggerated example in regards to the drop in collateral value, but play around with the numbers and the point that I am trying to make is clear. Even just a -10% deterioration in the collateral value would still cause a -$11,500,000 shortfall of the existing debt payoff under these circumstances. Not going to spell out the negative feedback loop today, but there is one within this scenario that exists. See how much fun we are having in the Real Estate world right now!

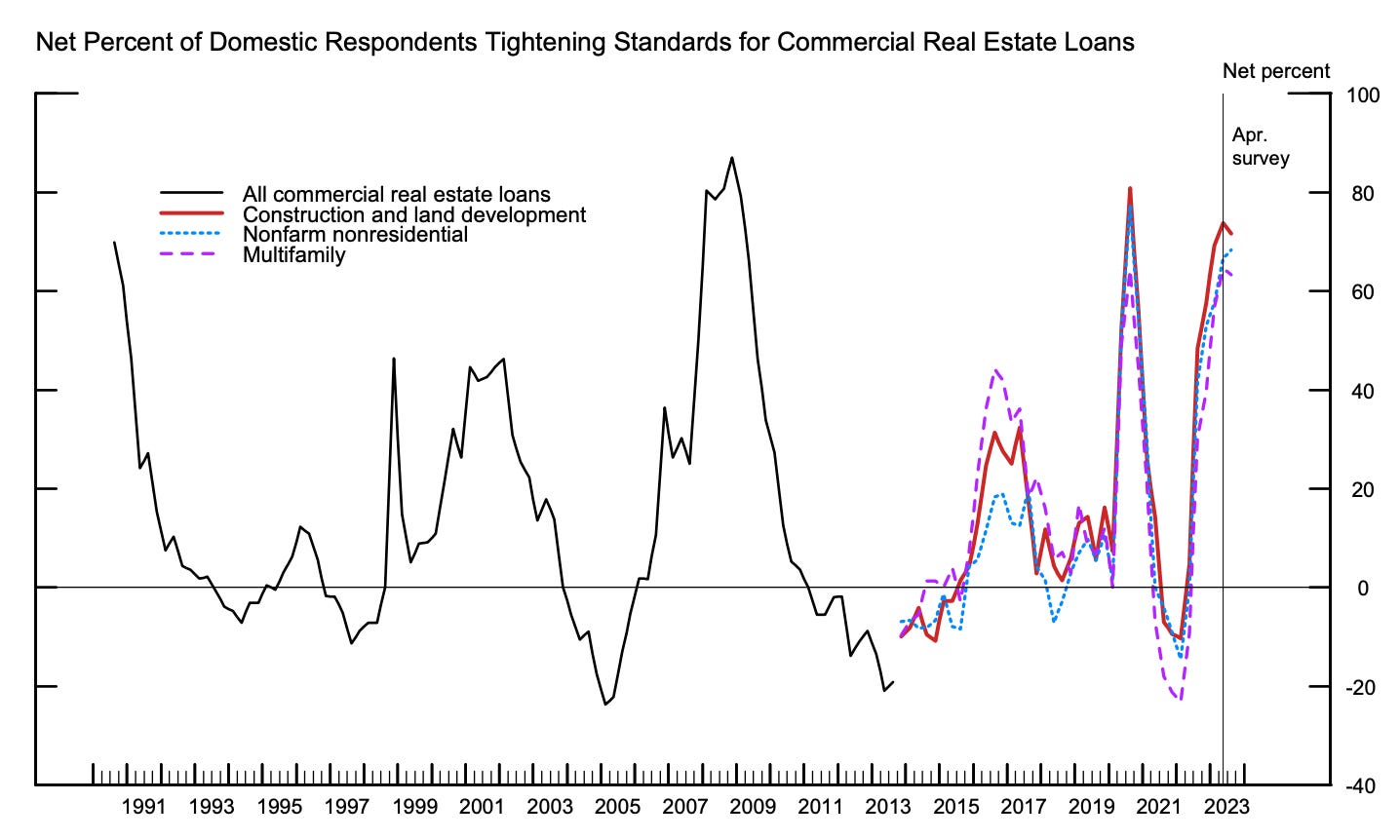

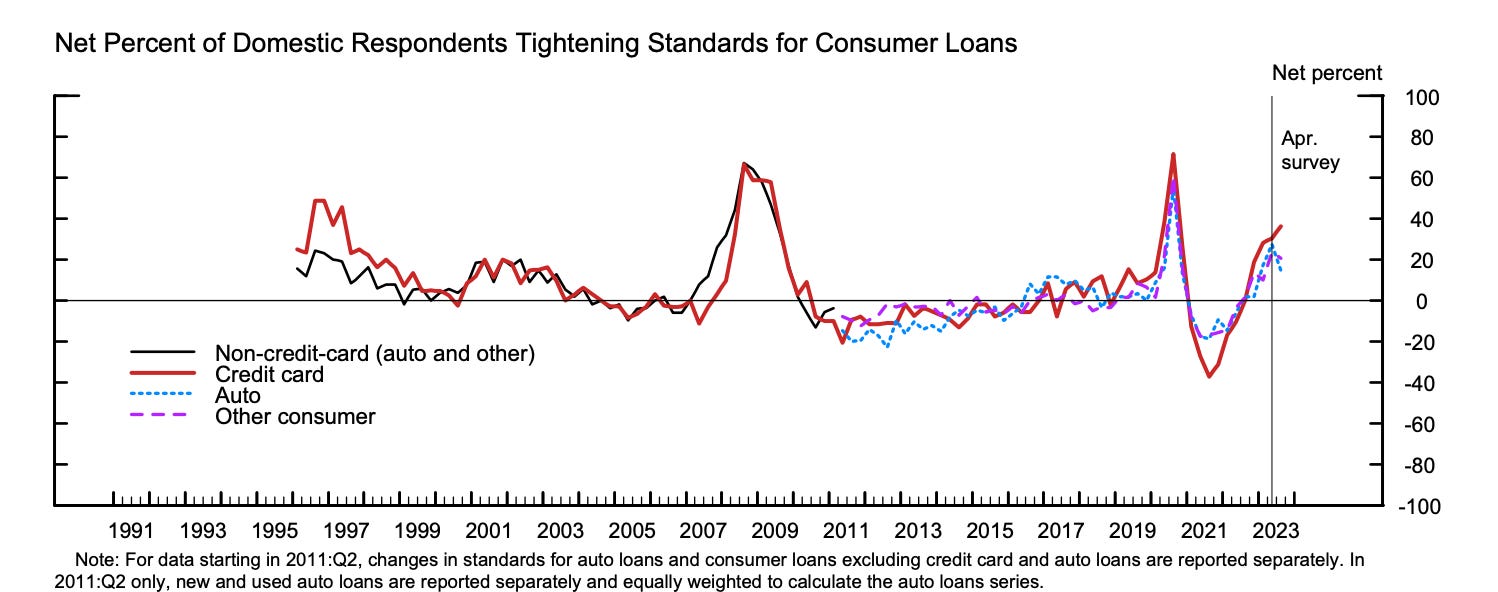

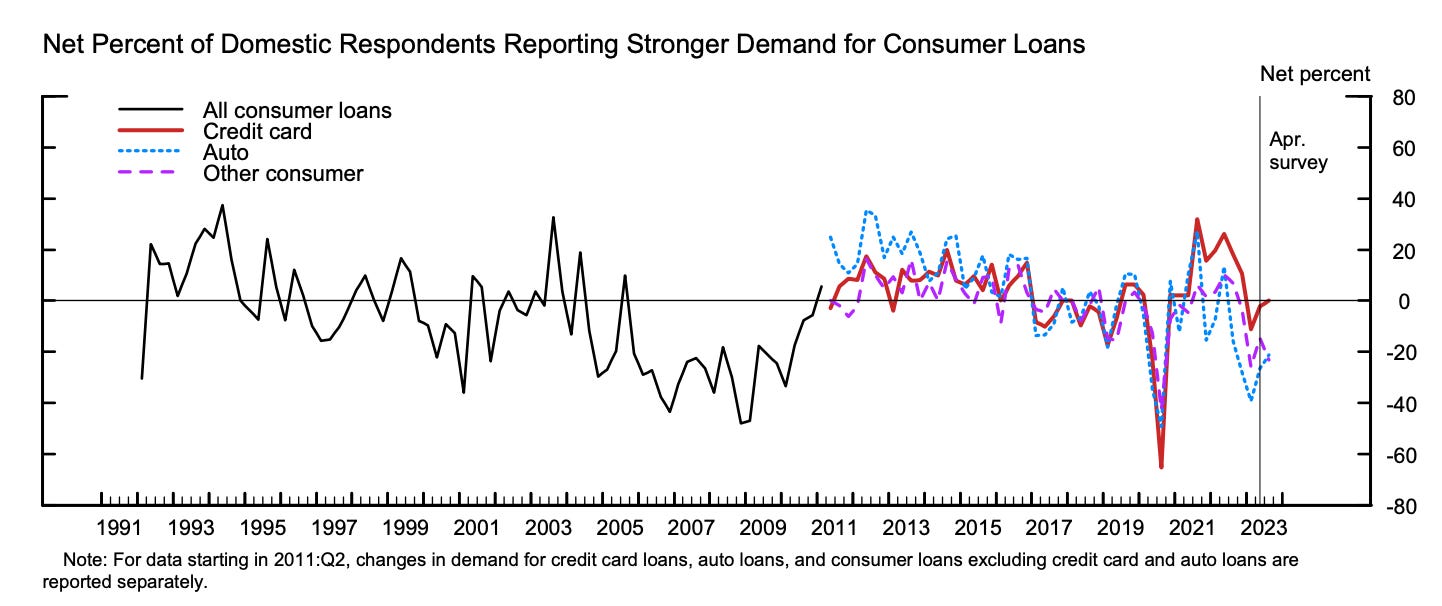

Below are some charts from the Senior Loan Officer Opinion Survey which exemplify the tighter credit standards and weaker loan demand. Overall, bank spreads increasing under tighter credit conditions. The cost of funds is going higher.

July 2023 Senior Loan Officer Opinion Survey (Higher spreads aka higher cost of capital)

July 2023 Senior Loan Officer Opinion Survey (C&I Loans)

July 2023 Senior Loan Officer Opinion Survey (Weak Demand for C&I Loans)

July 2023 Senior Loan Officer Opinion Survey (Tighter underwriting standards for CRE Loans)

No surprise to see the demand for commercial Real Estate loans slightly higher following the drop in treasury rates from March through June.

July 2023 Senior Loan Officer Opinion Survey (“stronger” demand for CRE Loans)

Similar to commercial Real Estate, no surprise in the increased demand for residential mortgages given the fall in treasury rates between March and June.

July 2023 Senior Loan Officer Opinion Survey (Stronger demand for residential mortgages)

July 2023 Senior Loan Officer Opinion Survey (Tighter credit standards for consumer loans)

July 2023 Senior Loan Officer Opinion Survey (Increased demand for consumer loans)

On the consumer side credit standards have steadily increased and this was reiterated by some of the commentary on the Discover and Capital One earnings calls. Consumer credit demand has risen off the lows, but this could be in part out of the necessity to keep spending and maintaining a former lifestyle.

The trend is clear for the tightening standards and loan demand for CRE and C&I lending. Remember the importance of credit growth impact as it translates to investment and real economic growth. Meanwhile, banks continue to increase spreads (the cost of funding is higher).

Going to offer a speculative thought here because it was interesting to me. Typically, I do not like to share thoughts or opinions that are not backed by data, but I want to share in the event that any readers would like to have an open discussion. I am also saying this with rates back at their cycle highs, so in my opinion the thought is poorly timed and it is easy to say this right now.

Have we seen a secular shift in interest rates? Imagine a world where rates are higher because of actual supply and demand. I understand that overall loan demand is weaker, but eventually, there will be a higher demand for debt, especially as the old debt begins to mature at a much larger scale. People still need debt, however, credit standards are tighter and credit is less available. What happens when the supply of something is constricted? It becomes more expensive.

The traditional recession playbook is to buy bonds for when the economy tank and government intervenes causing rates to fall precipitously. Everyone has known that to be true for years. I tried this trade multiple times myself and it didn’t work. I even discussed this as an asymmetric trade on this Substack under the caveat of the MOVE Index (bond volatility) breaking down. The MOVE did not break down, so I cut the cord on that idea on 7/19/23. The market has been trained over the last 20 years for an environment “where rates will always go lower”. Perhaps they will eventually and what I am saying is poorly timed.

The US Fed had a small window of time to tank the market into that type of environment, but instead along with the treasury they both added liquidity to the markets, blew up asset prices, and ran up the deficit into slowing economic growth. It is possible that we’ve passed that window in time for the “old playbook” to work. How long can the government intervene before there are consequences for their actions? Nature seeks equilibrium, whatever that may be.

Back in the late 1800s and early 1900s, most of the banking panics (markets crashed) also were characterized by rates increasing dramatically because credit and US dollars became so inaccessible that the costs to borrow were extraordinary. Banks would not lend to one another because of the counter-party risk. Given the negative M2 year-over-year comparisons between now and those periods of time, it has remained a point of intrigue for me to think about. All that being said, the Fed was created as a lender of last resort to prevent those types of baking crises from occurring. It is also worth mentioning, that it is unsustainable for the US government to run the deficit with rates at these levels, which would act as a counter point to “the secular shift in rates. Just thoughts.

Conclusion

Not much has changed on the macro side. The data has remained weak and, in many cases, has gotten worse. Apple reported the third straight quarter of lower sales volumes makes me consider how long certain companies will be able to hold pricing power. They are not the only company to be seeing this type of market dynamic. Credit to Mike Taylor, Simplify Asset Management for this thought.

Extend and pretend is the name of the game? How long can this type of behavior continue in the debt markets? The cycle seems to be moving at a glacial pace and numbers for Real Estate deals simply do not work right now.

Credit standards are tighter and the cost of capital is higher. This impacts borrowers’ abilities to refinance their existing debt. If collateral values fall further then that poses an even greater threat specifically in the Real Estate markets.

Imagine a world where rates are higher because of actual supply and demand. People still need debt, however, credit standards are tighter and credit is less available. What happens when the supply of something is constricted? It becomes more expensive.

In the meantime, there are going to be weeks where the market is up and others where it is down. Everything needs to be done incrementally. Getting a 5% yield on holding cash is great under the current set of circumstances. There are opportunities on both sides of the long and short book. After the market has gone down in a straight line for a week, it is appropriate to book “some” gains on the short side and add to some of the longs where it makes sense. Most importantly, maintain liquidity. Keep risk managing appropriately because it is going to be difficult to determine “when the music’s over”- Jim Morrison.

Happy Friday,

Aaron David Garfinkel

Resources

Senior Loan Officer Opinion Survey (Link)

Senior Loan Officer Opinion Survey Charts (Link)

Senior Loan Officer Opinion Survey Commentary (Link)

Mike Taylor (Twitter Link)

“When The Music’s Over”- Doors

Very insightful as always!