Game Theory

Let's discuss decision-making and how the recent re-acceleration of inflation is a significant external factor that influences a powerful individual decision-maker.

Highlights

Inflation Re-accelerating (at least for now). Meanwhile, Core CPI has remained sticky and persistent only falling from +6.6% (September 2022) to +4.7 (July 2023).

Headline CPI went from 9.1% (June 2022) to 3% (June 2023). During this time, the energy complex went deflationary and was one of the major disinflationary forces for the overall CPI index. However, one of the largest disinflationary factors has reversed.

These highlighted dynamics heavily impact the judgment of a powerful decision maker, the US Fed. The “higher for longer” monetary policy threatens sustainable economic growth and poses risks to companies with high leverage and debt-dependent industries such as commercial real estate.

Sunday Read! Better Late Than Never

There are decisions that impact the self such as “What time am I waking up” and there are decisions that influence the external world. In the case of the US government and the centrally controlled monetary policy, their actions affect the lives of +330 million people. This number is much larger if counting the lives of all the people around the world who are also dependent upon US economic prosperity. Unfortunately, it is difficult to envision a world in which these “

decision-makers” act in the best interest of the everyday hard-working US citizens. For these reasons, it is important to be proactively prepared for various challenges and understand why policy decisions are made along with the ramifications before such an event is voiced to the public.

What is Game Theory? “A framework for analyzing and understanding the behavior of rational individuals or entities (referred to as "players") when they are faced with decisions that involve competing interests. Game theory provides valuable insights into human decision-making and has practical applications in understanding and predicting behavior in competitive or strategic situations”- Chat GPT.

Thanks for the assistance above Chat GPT. I wanted to include “Game Theory” in today’s discussion because points in cycle time matter and that is why the recent 2-3 month re-acceleration of inflation is relevant. The timing of an upcoming decision and the influence of external factors are significant.

What is the decision that involves competing interests?

Kill inflation, but send the economy into an economic recession where there is mass unemployment for a period of time. The market is not happy.

Maintain slower economic growth, but inflation re-accelerates and remains structurally embedded within society. The market stays happy in the immediate term, while wealth disparity continues to grow and the quality of life falls for everyday hard-working Americans.

What is the behavior and strategic situation being analyzed?

The Fed raises rates again in September.

The Fed holds rates in September (this is what the market wants).

The Fed reinforces hawkish rhetoric and stance of rates higher for longer.

The Fed acts dovish on the margin and acknowledges that monetary policy is sufficiently restrictive (this is what the market wants).

The November policy meeting is in play as well.

During last week’s publication, “Pavlovian Response” (link here), we discussed the prospect of inflation re-accelerating (again for now). This week, I will provide data to support those assumptions and why this is my current view. Going into last week, the market was pricing only a 7% chance for an additional 25bps rate hike at the September meeting (19th-20th). The data that I am presenting throughout this discussion leads me to conclude that the market pricing for another rate hike should be much higher than what is currently represented.

Longer-term inflation becomes more uncertain due to the prospect of an eventual real recession and the disinflation shelter component (1/3 of CPI) which faces challenging base effects from September 2023 to March 2024. However, in the immediate term, the re-acceleration of inflation heavily impacts the judgment of a powerful decision maker, the US Fed. My view is that a “higher for longer” monetary policy, while necessary to kill structural inflation and bad behavior resulting from policy decisions made post-GFC, threatens sustainable economic growth and poses risks to companies with high leverage and debt-dependent industries such as commercial real estate.

Macro Optics will be hosting its first weekly online live discussion for free this upcoming Tuesday, September 12th at 7:30 pm Eastern time zone. We will be speaking about the pertinent conditions affecting the macro environment and addressing relevant trade/ investment ideas along with appropriate risk management for upcoming “headline events”. If interested, sign up for the Macro Optics platform with the link here https://macro-optics.com/booking-6164.

Macro

Quick re-cap:

The price of Oil has been +28.7% since the end of June.

Gasoline prices (RBOB) are +26% from the end of June.

Overall, the CRB Index (commodities index) is +10% during this time period.

For the sake of this discussion, it is important to highlight the weighting of the overall CPI index.

Food: 13.4%

Energy: 6.95%

Commodities less food and energy commodities: 21.3%

Shelter: 34.7%

Transportation services: 5.9%

Medical Care Services: 6.3%

What is the CPI index? According to the BLS (Bureau of Labor Statistics), “The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a representative basket of consumer goods and services. The CPI measures inflation as experienced by consumers in their day-to-day living expenses. Indexes are available for the United States and various geographic areas. Average price data for select utility, automotive fuel, and food items are also available. CPI indexes are used to adjust income eligibility levels for government assistance, federal tax brackets, federally mandated cost-of-living increases, private sector wage and salary increases, poverty measures, and consumer and commercial rent escalations. Consequently, the CPI directly affects hundreds of millions of Americans”.

Energy is one of the larger singular categories. Notably, the price of energy is contagious to other components within the index because it can impact various input costs. Energy can often front-run food prices as well. While a singular factor cannot be fully relied upon for total predictive value, it is worth noting the influence that the energy complex historically maintains over the CPI index. Dating back to 2000, the price of Oil has a positive correlation coefficient (R^2) of 0.4 in relation to the overall CPI index. This is a weaker positive correlation, but the correlation exists nonetheless.

Today, the discussion will be around the energy component for two main reasons. As mentioned above, there has been a substantial reflation of energy prices over the past month and a half. From the peak a year ago, CPI went from 9.1% (June 2022) to 3% (June 2023). During this time, the energy complex went deflationary and was one of the major disinflationary forces for the overall CPI index. Changes within the energy and Oil complex generally lead the reported data by approximately 1-month. Below are some charts that show the CPI index from the peak in June of 2022 and the year-over-year change for various energy components.

*Source: US Bureau of Labor Statistics

*Source: US Bureau of Labor Statistics

*Source: US Bureau of Labor Statistics

Above, the chart denotes year-over-year change in price for various categories for the index from July 2023. The energy component was a deflationary -12.5%, however an acceleration from the June low of -16.7%. While headline CPI fell precipitously over the last year with the energy complex as a driving force, Core CPI has remained sticky and persistent only falling from +6.6% (September 2022) to +4.7 (July 2023).

*Source: Tradingeconomics.com

Core CPI still remains well above the Fed’s 2% target which was once again reiterated during this past month’s meeting in Jackson Hole. Energy is very volatile, so often the Fed officials prefer to look at Core CPI, which is the overall index less food and energy.

As shown above, there has been little movement within the Core index. Given the majority of the headline disinflation has come from the energy and food components, the recent reflation in energy prices warrants additional attention. Below are three charts that I have built with data pulled from the BLS and Yahoo Finance. Charts 2 and 3 use the color Orange for CPI and Blue for Oil rate of change because GO GATORS! Chart 1 used the current prices of Oil going into next week.

Oil Rate of Change (Chart 1).

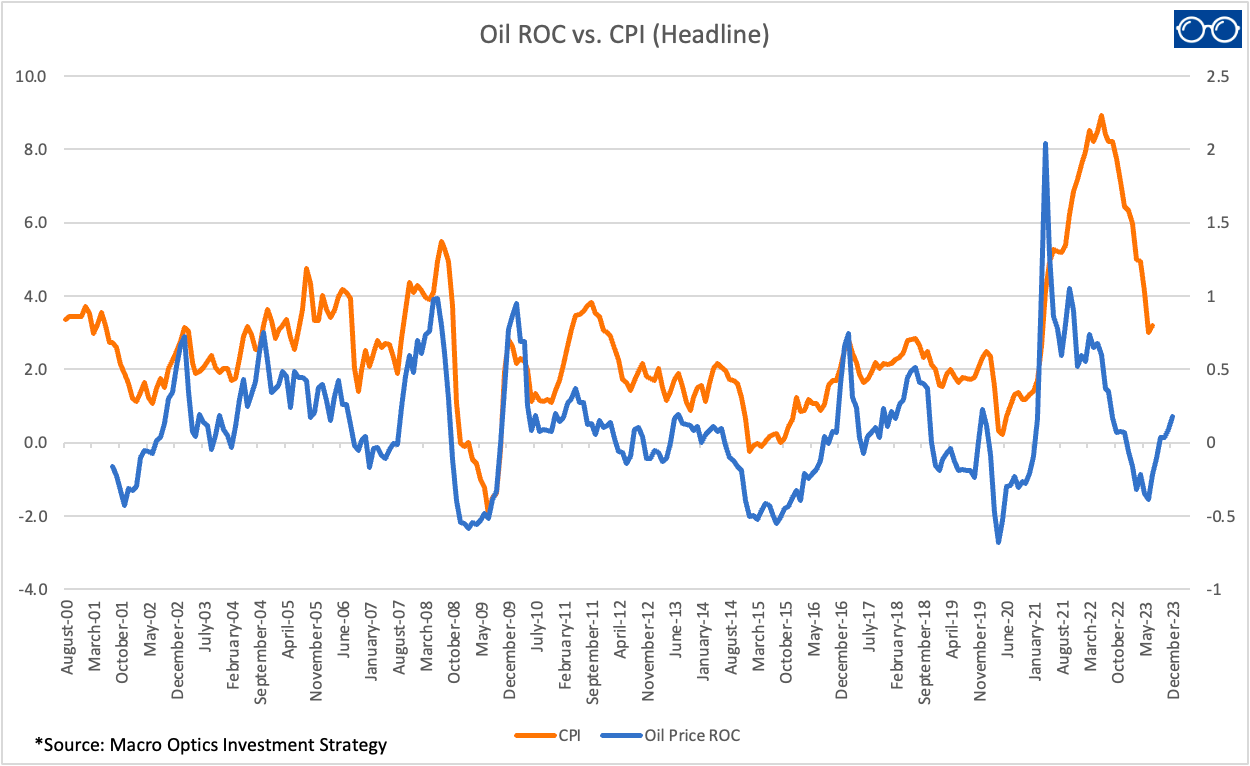

Oil Rate of Change (1-YR) vs. Headline CPI (Chart 2).

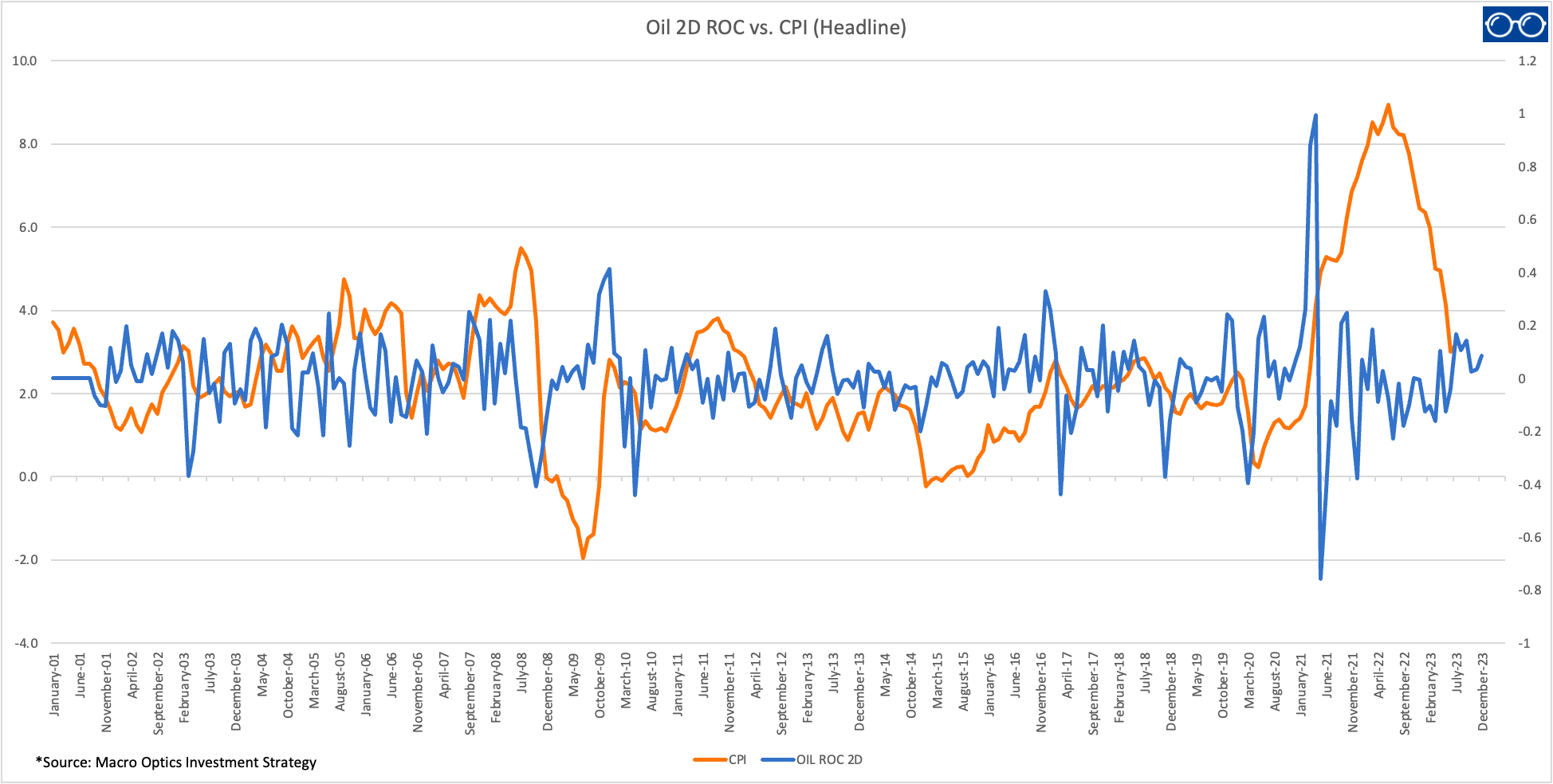

Oil Rate of Change (1-YR) in the second derivative vs. CPI (Chart 3).

The following assumptions were used in this analysis. I want to make it very clear that I am not making price predictions for Oil. For Charts 2 and 3, the following was used as a placeholder value to create a more complete image of the current trajectory in price rate of change terms. All values in the data set are actual historical prices except for the months of September, October, November, and December. For the placeholder months, starting with September, I have taken the average price history for the current daily prices for the month of September and used it as the monthly value of $86.5. In case the price trend is sustained, I have used the price of $90 in October, $92 in November, and $90 in December.

*Source: Data Yahoo Finance; Macro Optics Investment Strategy (Chart 1)

As shown above, the price of Oil began to bottom in the rate of change terms in May and June of 2023. By the end of July, the price rate of change was accelerating off the flows and the end of August shows a rate of change inflecting positively for the first time since December of 2022. The 2-YR rate of change of the price inflected positively in June and moved deeper into positive territory at the end of August.

*Source: Data Yahoo Finance and BLS; Macro Optics Investment Strategy (Chart 2)

The chart above demonstrates the relationship between the price of Oil and Headline CPI. As previously discussed, dating back to 2000, the price of Oil has a positive correlation coefficient (R^2) of 0.4 in relation to the overall CPI index. This is visible above as the peaks and troughs of CPI and the price of Oil often coincide with one another. The price rate of change of oil often leads the reported data within the overall CPI index.

*Source: Data Yahoo Finance and BLS; Macro Optics Investment Strategy (Chart 3)

The leading nature of the Oil price rate of change is apparent when viewed in the second derivative. While the blue line often remains in a tight range of motion, the exaggerated movements of the blue line are noticeable. These are substantial events in rate of change terms where there is a larger divergence between the relationship of the blue and orange lines such as years 2002, 2003-2004, May 2008, May 2009, 2011, 2015, 2018, February 2020, and June/ November 2020. Many of these years coincide with sizable accelerations or decelerations for the headline CPI index.

June to July has already shown an acceleration off the lows in the energy complex based on the reported CPI data. Five of the seven categories accelerated during the month of July. The majority of the components below are still negative, however less negative.

*Source: BLS; Macro Optics Investment Strategy

Based on the data that we have been analyzing above, there is a strong likelihood of seeing this short-term trend extend into the reported data for the months of August and September. Remember, the energy complex usually flows into the reported data at a one-month lag. When making the final decisions, the Fed has reiterated the “data dependent” stance and how they are continuing to look at the “new” data as it is released. Many of these data points that the Fed is using to make their ultimate choice such as CPI, PCE, and Headline non-farm payrolls are lagging indicators. This is why it is critical to understand behavior in competitive or strategic situations. Additionally, there will be a rate decision in November where a sustained trend in the recent reflation of energy prices stays relevant. The models that I have built above are in an effort to front-run those reports and the Fed.

Conclusion

As discussed above, the goal of this conversation is to consider the external factors that are influencing a much larger choice being made by a powerful decision-maker. Going into last week, the market was pricing only a 7% chance for an additional 25bps rate hike at the September meeting. The data that I am presenting above leads me to conclude that the market pricing for another rate hike should be much higher than what is currently represented.

Inflation Re-accelerating (at least for now). Meanwhile, Core CPI has remained sticky and persistent only falling from +6.6% (September 2022) to +4.7 (July 2023).

Headline CPI went from 9.1% (June 2022) to 3% (June 2023). During this time, the energy complex went deflationary and was one of the major disinflationary forces for the overall CPI index. However, one of the largest disinflationary factors has reversed.

These highlighted dynamics heavily impact the judgment of a powerful decision maker, the US Fed. The “higher for longer” monetary policy threatens sustainable economic growth and poses risks to companies with high leverage and debt-dependent industries such as commercial real estate.

I want to reiterate that I do not actually know what is going to happen. Orange is only a good color for me when I am in the swamp. However, what I am presenting is an opportunity where there are many market participants who could get caught offside. It is always important to highlight asymmetric market setups. Remember, it was only a month and a half ago in early July when the financial press and broad market participants were celebrating, “The end of inflation”. Investors and markets do not like surprises. High-yield spreads continue to be discombobulated from rising bankruptcies and the Vix remains at complacent low levels. Specifically for the next two weeks, I maintain a broad stance that it is prudent to reduce gross US equity exposure into strength and continue raising cash that is earning +5%.

Lastly, Macro Optics will be hosting their first weekly online live discussion for free this upcoming Tuesday, September 12th at 7:30 pm Eastern time zone. We will be speaking about the pertinent conditions affecting the macro environment and addressing relevant trade/ investment ideas along with appropriate risk management for “headline events”. If interested, sign up for the Macro Optics platform with the link here https://macro-optics.com/booking-6164.

Good Luck,

Aaron David Garfinkel

Resources

Macro Optics (https://macro-optics.com)

Yahoo Finance (Oil Price Data)

CPI Bureau of Labor Statistics (BLS)

Tradingeconomics.com (Core Inflation)

The Oil ROC vs CPI comparison is a great observation